Robert Kelly, Chief Economist, Central Bank of Ireland

What is the outlook for the Irish economy?

The Middle East conflict has been pushing energy prices higher, worsening the inflation outlook and affecting household spending.

However, exceptionally strong business investment, particularly in AI and data centres, is offsetting these headwinds.

This has led to us revising our domestic growth forecast upwards to 3.3 per cent for 2026 and in the region of 3 per cent annually out to 2028.

The reported Middle East peace deal would materially improve the inflation outlook.

However, the economy must still absorb existing shocks. For example, food prices will continue reflecting higher fertiliser costs as this year's crops mature.

If the peace deal doesn’t hold and creates prolonged energy disruptions, inflation could approach 5 percent and push domestic growth below 2 percent next year.

What does the economic outlook mean for government spending and taxation?

Ireland's national development plan faces new cost pressures as construction prices rise sharply.

Prioritising investment in digital infrastructure, roads and energy networks could help offset rising costs, attract private business investment, and strengthen Ireland’s long-term competitiveness.

More broadly, over the last five years, public spending has grown by nearly 10 per cent per year. This is well above the rate the economy can sustain, and it is set to continue at a strong pace.

This spending growth is increasingly being financed by excess corporation tax. A sudden decline in these tax revenues could create a 13.5 billion euro shortfall in the public finances by 2028.

With so many competing demands, an effective fiscal anchor would enable policy flexibility while preventing uncontrolled spending growth.

Find out more:centralbank.ie/QB

Comment

The global economy continues to face challenges and heightened uncertainty arising from the conflict in the Middle East, with the disruption in the Strait of Hormuz continuing into its fourth month. Going in the other direction, continued AI-related capital investment has supported global economic activity, and this has also been evident in the Irish economy. Even when the conflict is fully resolved the restoration of supply chains will take an extended period. Accordingly, there has been exceptional volatility in spot oil prices alongside related commodities and more persistent challenges to supply leading to a higher outlook for energy prices generally. For Ireland, higher energy costs are eroding household real incomes and dampening consumer confidence, while also feeding through to broader inflationary pressures. The conflict poses complex risks to global supply chains beyond energy, with potential downstream effects on production costs and economic activity. Against this backdrop, domestic economic policy faces the dual challenge of supporting those most vulnerable and enabling households and firms build resilience to these shocks generally, while avoiding measures that unnecessarily add to demand or entrench inflationary pressures within the economy.

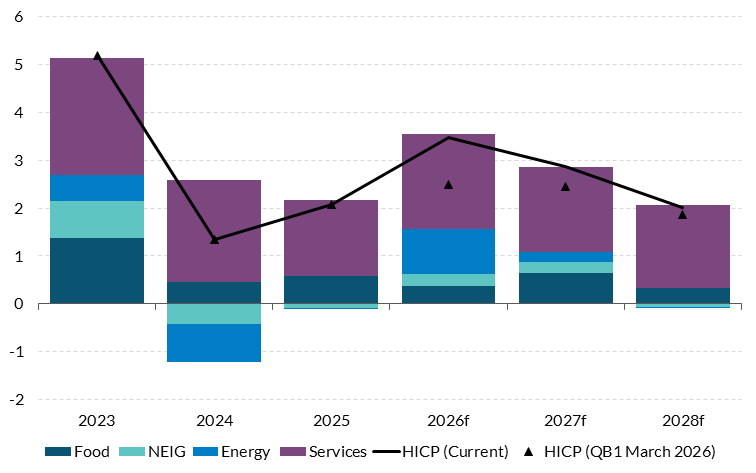

These developments have led to material changes to the economic outlook that prevailed before the conflict, with somewhat divergent views on consumer spending and business investment, especially in 2026. Modified domestic demand (MDD) growth is projected to moderate, reflecting the damping effects of higher energy prices on real incomes and consumption. However, the momentum in MNE-led investment is expected to be significant in contributing to overall MDD growth over the forecast horizon. Inflation forecasts have been revised upwards notably, to 3.5 per cent this year and 2.9 per cent in 2027, with the outlook for energy prices substantially higher than assumed in the March Bulletin. However, uncertainty around these baseline projections is exceptionally high, and risks remain firmly tilted to the downside for growth and to the upside for inflation.

Given the scale of uncertainty, this Bulletin presents alternative scenarios to illustrate the range of possible outcomes. In the milder scenario, where the conflict is resolved swiftly, oil and gas prices fall below those expected in our baseline forecast, supporting slightly stronger growth and lower inflation. However, even in this scenario, the effects of the disruption already experienced since the start of the war continues to exert upward pressure on inflation relative to what was expected prior to the conflict. In the severe scenario, energy and food commodity prices are assumed to remain persistently higher, inflation would reach materially elevated levels, approaching 5 per cent in 2027, while growth would slow significantly. Beyond direct energy price impacts, the conflict also presents broader global supply chain implications (Box C). Energy-intensive products produced in the Gulf region, such as fertilisers and helium—the latter a critical input in semiconductor fabrication—have seen sharp price increases with downstream implications for consumer prices. An escalation could trigger more extensive disruptions not fully captured in the scenarios published in this Bulletin. These effects differ markedly across sectors: multinational enterprises face heightened uncertainty around input costs and export demand, while indigenous firms may have more limited ability to absorb rising input costs, and households are more directly exposed to cost-of-living pressures.

Against this uncertain backdrop, the preliminary national accounts data for Q1 2026 epitomised the dual nature of the Irish economy. MDD grew strongly, heavily influenced by multinational-dominated investment, particularly in AI and data centre-related capital goods. In contrast, headline GDP contracted sharply during the quarter, reflecting base effects from the volatile swings in exports of polypeptide hormones last year and a contraction in offshore goods trade. These divergences underscore the necessity of looking beyond headline measures to understand underlying momentum in the domestic economy.

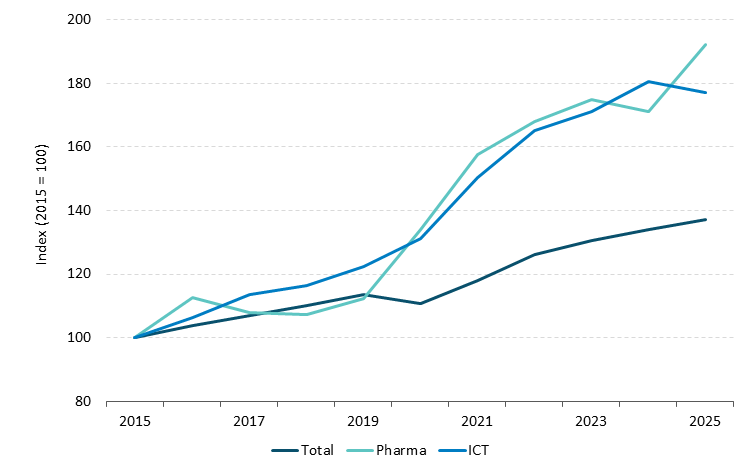

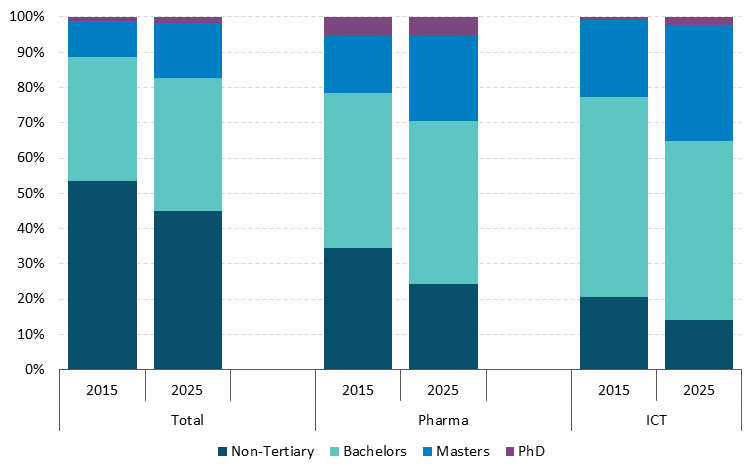

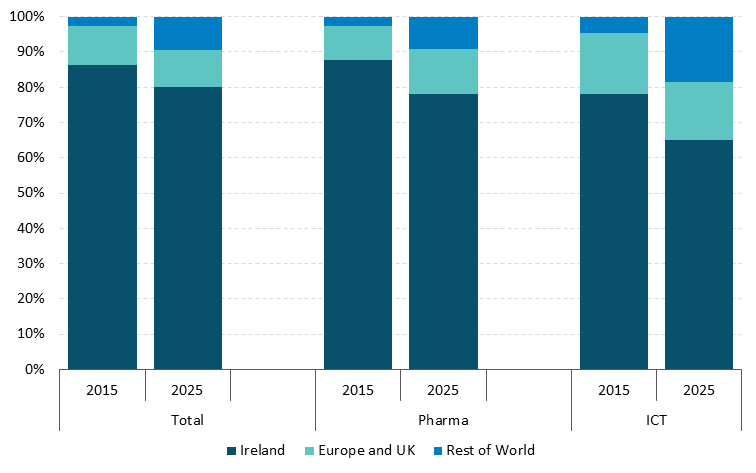

MNEs continue to play an outsized role, not only in investment and exports, but also in tax revenues, while they are prominent in the labour market as well. The pharmaceuticals and ICT sectors have been significant drivers of employment growth in recent years, particularly for workers with advanced qualifications (Box B). The share of workers with tertiary-level qualifications has increased substantially over the past decade, partly driven by these MNE sectors. The sectors differ markedly in international recruitment patterns, with ICT relying more heavily on workers from beyond the EU. These sectors also contribute disproportionately to corporation tax revenues, with ICT and pharmaceuticals together accounting for over half of all CT revenue, up sharply since 2019. This concentration creates significant fiscal vulnerabilities, particularly given volatility and uncertainty around future investment and employment trends in these globally mobile sectors.

The strength in MDD through 2025 and into early 2026 was underpinned by robust investment, particularly in AI and data centre-related activity. AI-linked data centre hardware imports have surged in recent years to represent over half of modified machinery and equipment investment (Box A). The scale of this investment activity, combined with strong overall employment growth in recent years, has maintained the economy performing at close to its potential by early 2026. However, the labour market is now showing signs of softening. Employment growth is moderating, job postings have continued to decline, and the unemployment rate has increased marginally. Expectations around real wages have declined, with nominal wage growth not expected to keep pace with inflation in the near-term, contributing to a deterioration in consumer confidence. Personal consumption growth is expected to be more subdued as higher energy prices continue to erode real household disposable incomes. This represents a different context compared to the previous energy price shock following the Russian invasion of Ukraine, when the labour market was tightening, adding to nominal wage growth at that time.

Energy price growth has been revised upward sharply following increases in wholesale oil and gas price assumptions and announced utility price rises. Direct effects are clearly visible in headline inflation, with energy contributing significantly. However, there is also evidence of indirect effects as higher energy costs feed through to production costs across goods and services, with transport costs increasing and prices for energy-intensive products rising sharply. Services inflation has remained elevated, partly reflecting the pass-through of higher input costs but also continued domestic demand and wage pressures. The key risk is the potential for second-round effects to emerge, whereby workers seek compensation for real wage erosion through higher nominal wage demands, and firms pass through these higher labour costs to consumer prices to maintain profit margins. While there is no evidence of widespread second-round effects to date, the risk remains significant, particularly if the energy shock proves more persistent or if the conflict escalates further.

At the euro area level, monetary policy has responded to heightened inflationary pressures to ensure euro area inflation stabilises sustainably at the 2 per cent medium-term target. In June, the ECB Governing Council raised its three key interest rates, by 25 basis points. The policy tightening is motivated by the sharp increase in energy prices and their indirect effects on broader inflation. The Governing Council’s policy deliberations remain data-dependent, with the Council continuing to assess incoming information on a meeting-by-meeting basis.

From a domestic policy perspective, the priority must be to strengthen the resilience and sustainability of the public finances while supporting the economy's adjustment to the energy shock. As highlighted in a Signed Article (PDF 1.01MB) accompanying this Bulletin, recent years have seen substantial increases in recurring government expenditure alongside a growing dependence on corporation tax, which now accounts for nearly one-quarter of total government revenue. When estimated excess corporation tax is excluded, the underlying budget deficit has increased substantially. Expenditure growth has exceeded initial budget plans over the last five years resulting in overall government spending growing at rates well above what would be consistent with the economy's estimated sustainable capacity. The absence of an effective fiscal anchor remains a significant concern. Committing to a credible expenditure rule that aligns spending growth with the economy's trend growth rate is essential for establishing effective counter-cyclical fiscal policy and placing the public finances on a sustainable path. This is particularly important given structural pressures from population ageing, infrastructure needs, and vulnerabilities from tax base concentration. With the economy operating close to capacity, budgetary policy should not add further demand stimulus at present. Any additional support measures for vulnerable households should be targeted and tailored, and accommodated within existing budgetary allocations. At the same time, addressing vulnerabilities from the narrow tax base would be complementary to maintaining macro-financial stability, with a broad range of possibilities from reviewing tax reliefs, consumption and property taxes and social insurance contributions among the feasible options.

Beyond fiscal discipline, addressing supply-side constraints remains critical for supporting sustainable growth and improving living standards. The economy faces binding constraints in housing, energy, water and wastewater, and transport infrastructure. These constraints are limiting current economic activity and reducing the economy's potential growth rate. Measures that reduce fossil fuel dependency would represent more sustainable support, helping to build resilience against future geopolitical shocks while contributing to emission reduction targets. A higher investment rate by households and indigenous firms being crowded in through appropriately funded and well prioritised public capital spending would sustainably support long-term growth. Planned expenditure under the National Development Plan is designed to address these shortages, and reforms such as those outlined in the Accelerating Infrastructure Report and Action Plan are welcome. However, translating these plans into actual delivery will require sustained effort, effective project management, and willingness to address longstanding bottlenecks. With economic conditions still relatively favourable despite recent headwinds, a window of opportunity exists to improve the resilience of the public finances and the economy to the structural pressures and external shocks that lie ahead.

Outlook for the Irish Economy

Recent Developments and Forecast Summary

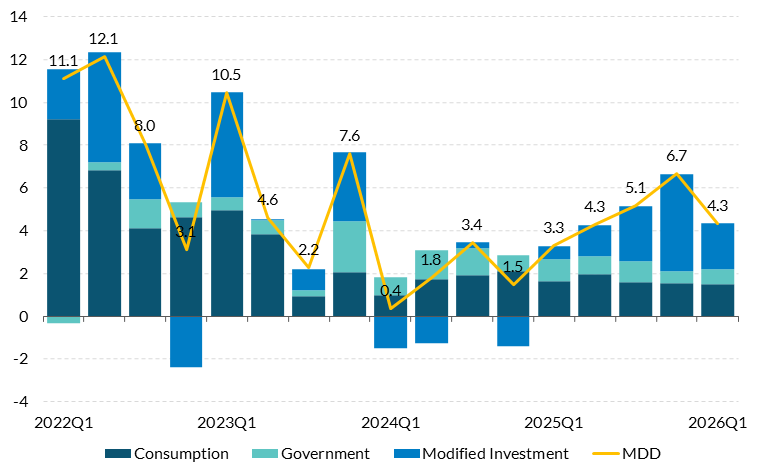

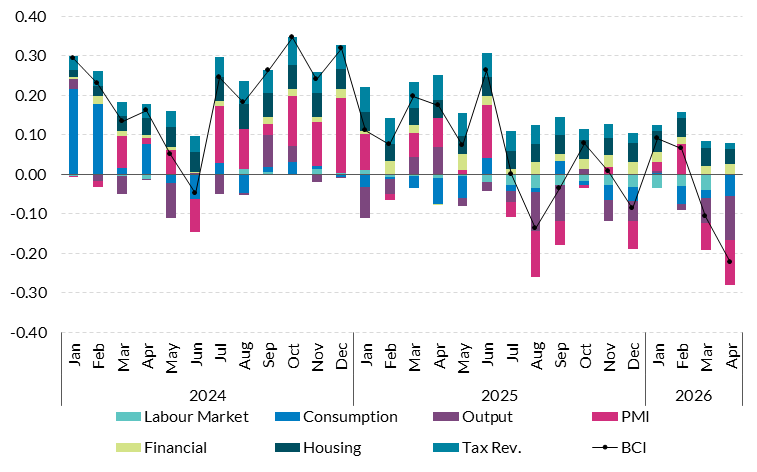

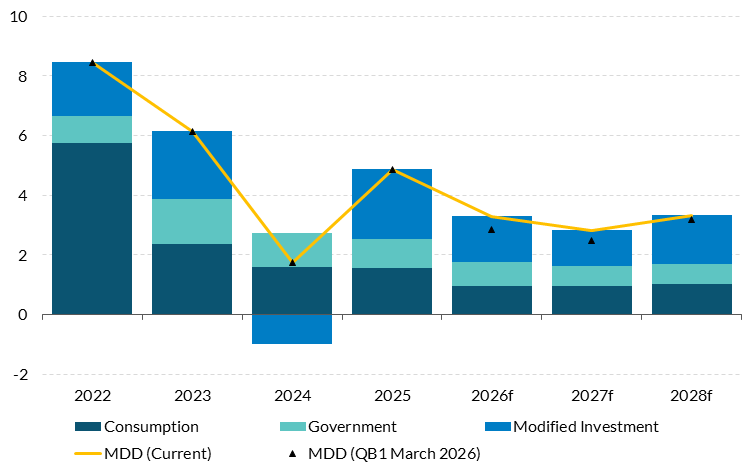

Continued strength in investment underpinned growth in Modified Domestic Demand (MDD) in the first quarter of 2026, though growing indications of a slowdown were evident in other more domestically-oriented indicators. Economic activity (Modified Domestic Demand) expanded by 4.3 per cent in Q1 2026 compared with the same quarter in 2025 (Figure 1). This strong pace of growth comes on the back of continued strength in modified investment, particularly related to AI and data centres by multi-nationals. Domestic building and construction investment increased by 4.9 per cent while multinational-dominated modified machinery and equipment increased by 16.6 per cent in the first quarter. More domestically oriented and less volatile indicators of growth in the Irish economy also point to continued growth in the first quarter of 2026 but suggest that the pace of growth is slower than indicated by headline MDD (Figure 2). Output of domestically-oriented sectors increased 1.4 per cent and growth in non-corporation tax revenue slowed to 5.5 per cent in the first five months of the year, down from 6.4 per cent for the same period last year. Consumption continued to grow at a steady rate of 2.6 per cent year-on-year in Q1, although recent retail sales and card payment data for April suggest a slight slowdown in consumer spending at the start of Q2, as the conflict in the Middle East may be becoming more evident in the data (Figure 11). The labour market picture is more complicated. The Labour Force Survey indicates no job growth in the first quarter relative to the previous year, a marked slowdown, while monthly payrolls do not indicate such a sharp slowdown in employment growth and unemployment has remained below 5 per cent. The Central Bank’s Business Cycle Indicator (BCI) summarises the information from the latest high-frequency monthly data, separating out the underlying trend in activity from movements due to noise. The latest BCI estimates indicate that the economy hovered around its long-run average rate of growth in Q1, but with a notable weakening in March and April. The main negative contributions to the BCI in March and April were traditional sector output, PMIs and weaker labour market data.

MDD grew strongly in the first quarter of 2026 on the back of modified investment, with consumption remaining steady

Figure 1: Contributions to year-on-year change in Modified Domestic Demand (MDD), (p.p.)

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

The BCI remained around its long-run average in Q1, but weakened in April

Figure 2: Business Cycle Indicator and Contributions, Average growth = 0

Source: Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Note: Details on the methodology underpinning the BCI available here (PDF 790.91KB). The zero axis corresponds to the long-run average historical growth rate in realised MDD. Deviations above or below zero therefore signify that activity is growing faster/slower than its historical average rate.

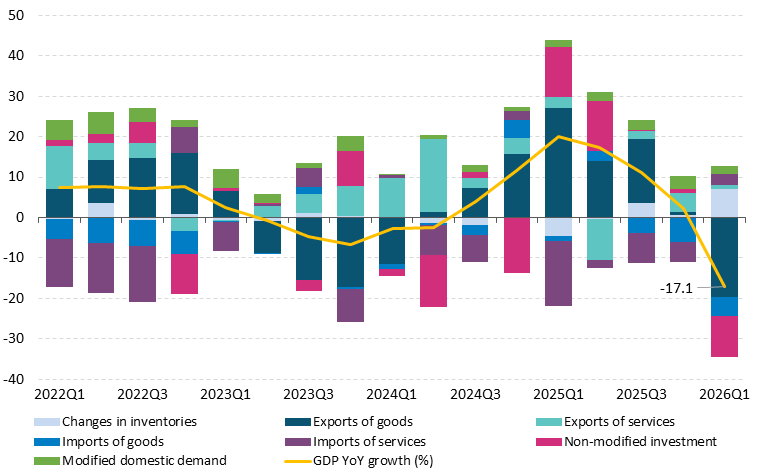

GDP fell by 17.1 (12.1) per cent year-on-year (quarter-on-quarter) in 2026 Q1, driven by a sharp drop in both polypeptide-hormone exports and net trade related to offshore goods. This was a significant negative surprise relative to the flash estimate of a 6 per cent decline released in April 2026. The reasons for the decline are concentrated in the pharmaceutical sector. Most of the year-on-year drop in GDP is explained by a sharp fall in both cross-border goods exports (which were exceptionally large in the first quarter of 2025) and MNE-related offshore net trade. The former is driven by the dynamics of exports of polypeptide hormones, a key component of weight-loss drugs, which were extremely volatile through 2025. While a large negative contribution to GDP growth due to 2025 base effects was expected, a disconnect between the volume and value of polypeptide hormone exports in March also contributed to the magnitude of the change (Figure 17). In addition, net trade related to offshore goods (merchanting and contract manufacturing), for which information is limited for the CSO flash estimate, both made large negative contributions to quarter-on-quarter GDP growth.

GDP fell sharply in the first quarter of 2026, highlighting its sensitivity to the (onshore and offshore) activities of a small number of multinational enterprises

Figure 3: Contributions to year-on-year change in Gross Domestic Product (GDP), (p.p.)

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

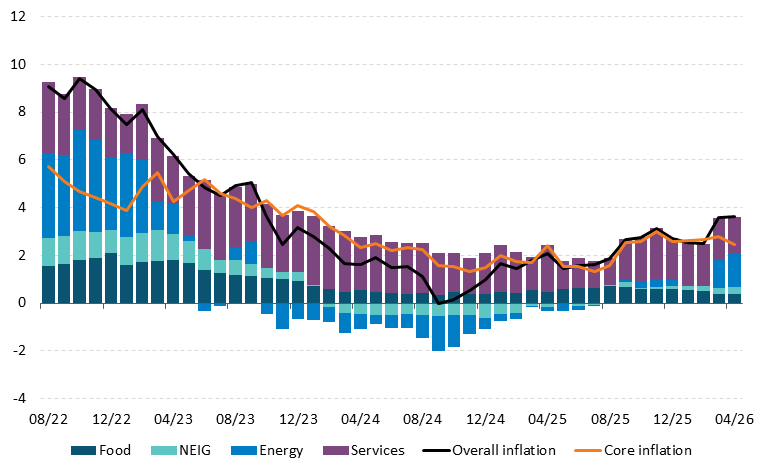

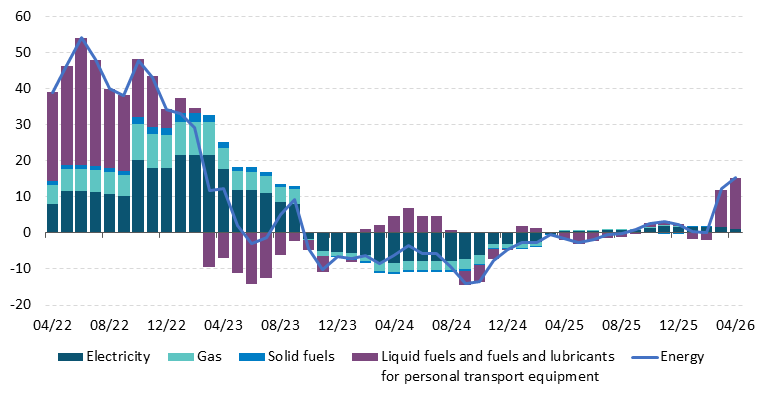

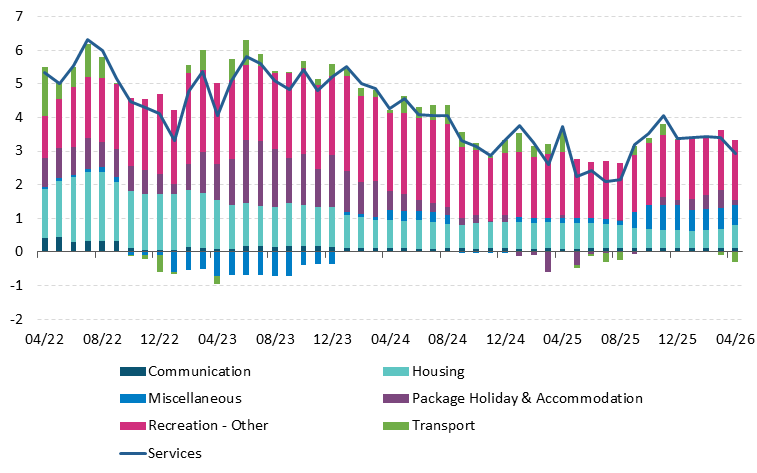

Headline inflation has picked up since March, driven by rising energy prices. Headline HICP increased, on a year-on-year basis, to 3.5 per cent in May with core inflation remaining stable at 2.8 per cent. Energy prices rose sharply in recent months, with April and May, recording increases of 15.3 per cent and 11.9 per cent respectively, contributing more than one percentage point to headline inflation. This pronounced upward momentum in energy prices stems primarily from liquid fuels (see Figure 4). Non-energy industrial goods (NEIG) showed a slight pickup in inflation in the first quarter, though food and services inflation remain stable so far. Underlying inflation measures have edged upwards, remaining above pre-pandemic levels.

Headline inflation rose in recent months, driven by energy price increases as a result of conflict in the Middle East

Figure 4: Contributions to headline inflation (year-on-year per cent change)

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Energy prices rose sharply in Q1 2026 driven by strong surge in Liquid Fuels

Figure 5: Contributions to energy inflation

Year-on-year per cent change (%)

Chart data in accessible format. (XLSX 164.97KB)

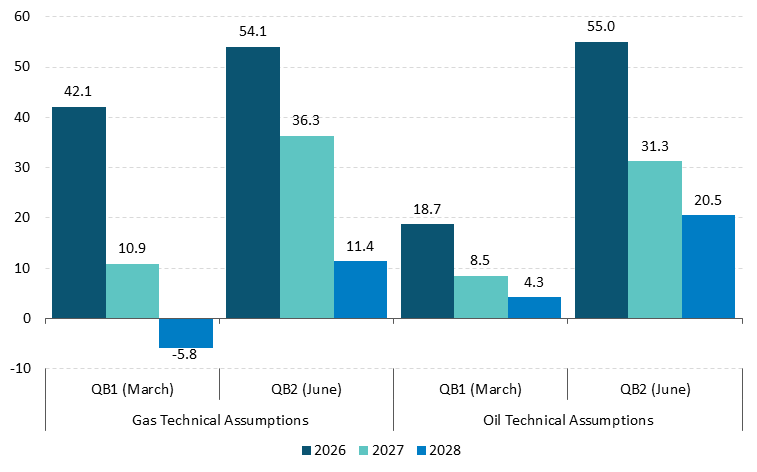

Modified domestic demand is projected to continue growing strongly, largely supported by investment, offsetting weakness in consumption due to higher energy prices. The central forecast is based on an assumed market-implied path for oil and gas futures prices as of mid-May 2026. The assumptions regarding the impact of the war on energy prices have been revised upwards since the previous Bulletin. Oil prices in particular are assumed to be 30.2 per cent higher on average in 2026 than in the March 2026 Bulletin assumptions, and 55 per cent higher than in the December 2025 Bulletin (Figure 6). Gas price assumptions for 2026 are up 12 per cent since the previous Bulletin, and 54 per cent since the December 2025 Bulletin. Driven by higher energy costs, projected inflation has been revised upwards to 3.5 per cent in 2026 and 2.9 per cent in 2027. This represents a revision from the previous Bulletin of 0.6 and 0.3 percentage points over the 2026 and 2027 period respectively (Figure 8). Higher inflation has prompted knock-on downward revisions to households’ real disposable income and consumption for 2026. On the other hand, the outlook for modified investment has improved, building on the momentum and broad-based growth in 2025. AI and data-centre related investments in particular are playing an increasingly important role (see Box A). The result is that overall MDD growth is being revised up marginally in 2026 and 2027, to 3.3 and 2.8 per cent respectively (Figure 7). The central projections are sensitive to the assumed path of energy prices and realised outturns on investment and imports of AI and data-centre related capital goods. An escalation of the conflict in the Middle East resulting in higher energy prices than assumed in the central forecast would lead to higher inflation and weaker growth (see Balance of Risks to the Outlook).

Further upward revision to energy price assumptions since the March 2026 projections

Figure 6: Energy price assumptions, QB2 2026 (June) and QB1 2026 (March) versus December 2025, annual percentage change

Source: ECB. Chart data in accessible format. (XLSX 164.97KB)

Note: The Synthetic Energy Commodity Price Index (SECPI) is a weighted average of oil and gas prices both expressed in USD/MWh.

MDD growth revised up on basis of strong investment offsetting somewhat weaker consumption due to high energy prices

Figure 7: Contributions to annual change in MDD (per cent)

Source: CSO, Author’s Calculations. Chart data in accessible format. (XLSX 164.97KB)

Energy prices and services drive headline inflation higher, projected to reach 3.5 per cent in 2026

Figure 8: Contributions to annual change in headline inflation (per cent)

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Volatility in goods exports is likely to continue in 2026, but overall net trade is projected to contribute positively to economic activity out to 2028. Consistent with the large drop in goods exports in Q1, merchandise exports are expected to fall overall in 2026 following the exceptional rise in 2025 due to exports of weight-loss related pharmaceuticals. However, there is significant uncertainty around the baseline projection (see Balance of Risks to the Outlook). Stripping out volatility associated with weight-loss pharma exports, solid global demand for the main outputs of the Irish pharma sector and the expected opening of new manufacturing capacity, contribute to the projection of sustained growth in merchandise trade out to 2028. Relative to 2025, exports are expected to rebalance towards services, with the latter also forecast to see robust growth on the back of strong ICT-related exports. Overall net exports of goods and services produced in Ireland is forecast to make a negative contribution to GDP growth in 2026, before turning positive out to 2028. Combined with the outlook for domestic demand, this underpins the forecast for growth in real modified national income (GNI*) of 3 per cent per annum on average from 2026 to 2028, slightly below the average expected growth in MDD over the same period (Table 1). The modified current account (CA*) is expected to remain in surplus throughout the forecast horizon.

Risks to the growth outlook remain firmly tilted to the downside, with significant uncertainty around the baseline. The first major source of uncertainty is the duration and severity of the conflict in the Middle East, with the Strait of Hormuz still mostly closed at the time of writing. The Balance of Risks to the Outlook considers adverse and severe scenarios in which energy and food commodity prices remain higher for longer relative to baseline assumptions. This would increase inflation and reduce growth in Ireland. Of note given the large drop in 2026 Q1 GDP, considerable uncertainty surrounds the path of exports and imports, due both to the inherent volatility of the recent onshore export/import drivers (polypeptide hormone exports and AI-related imports) as well as the offshore components of contract manufacturing and merchanting. Over the medium term, there are downside risks to Irish exports and corporation tax receipts if the US changes its corporate tax or industrial policy stance, with potential knock-on effects on investment and incomes. In addition, the pace of developments in AI-related technologies is extremely fast, though there is a lot of uncertainty about the nature and magnitude of their economic impacts, both in Ireland and globally. Finally, a further risk is that capacity constraints could become worse if progress on alleviating infrastructure gaps in the economy is delayed or inadequate.

Table 1: QB2 June 2026 Forecast Summary and Revisions from March 2026 Baseline Projections

| | 2024 | 2025e | 2026f | 2027f | 2028f |

|---|

Constant Prices | | | | | |

| Modified Domestic Demand | 1.8 | 4.9 | 3.3 | 2.8 | 3.3 |

| Modified Gross National Income (GNI*) | 4.8 | 4.7 | 2.4 | 3.0 | 3.5 |

| Gross Domestic Product | 2.6 | 12.3 | -2.7 | 6.5 | 4.0 |

| Total Employment | 2.7 | 2.2 | 1.2 | 2.0 | 1.8 |

| Unemployment Rate | 4.3 | 4.7 | 5.1 | 5.2 | 5.2 |

| Harmonised Index of Consumer Prices (HICP) | 1.3 | 2.1 | 3.5 | 2.9 | 2.0 |

| HICP Excluding Food and Energy (Core HICP) | 2.3 | 2.0 | 3.0 | 2.8 | 2.3 |

Revisions from previous Quarterly Bulletin (percentage points) | | | | | |

| Modified Domestic Demand | 0.0 | 0.0 | 0.4 | 0.3 | 0.1 |

| Gross Domestic Product | 0.0 | 0.0 | -4.0 | 2.2 | -1.2 |

| HICP | 0.0 | 0.0 | 0.6 | 0.2 | 0.1 |

| Core HICP | 0.0 | 0.0 | 0.6 | 0.3 | 0.1 |

Forecast Detail

External Environment

The continued closure of the Strait of Hormuz, now in its fourth month, is having persistent negative effects on the world economy. The closure is causing significant disruption to the world economy by restricting the supply of oil and liquified natural gas (as well other important commodities, such as fertilizer, see Box C). Several emerging market economies have already started implementing policies to contain the demand for fuels, including, in some cases, rationing. In advanced economies, including the net energy-importing euro area, consumers have seen the increase in energy prices adversely affecting their purchasing power. OECD projections predict that global GDP growth will fall this year to 2.8, a reduction of 0.6 percentage points compared to the forecast before the start of the conflict. The sharp rise in energy prices has led to a resurgence in inflation (e.g., inflation reached 3.2 per cent in the euro area and 4.2 per cent in the US in May).

Despite the oil shock, major world economies continue to grow. Optimism about the impact of AI, combined with extraordinary levels of AI-related investment, have propelled the US stock market to new highs and provided a large boost to the US economy. The continued strong performance of US growth depends however on the eventual materialisation of AI-related productivity gains. US GDP grew at an annualised rate of 1.6 per cent (0.4 per cent Q-on-Q) in the first quarter, over half of which was due to growth of investment in information-processing equipment. Robust consumption growth, especially among wealthier households, can also in large part be attributed to the strength of the stock market. Meanwhile, monthly real income growth has been negative since March, as a result of the rise in fuel prices, while the unemployment rate has remained steady at around 4.3 per cent. The euro area economy grew by 0.2 per cent in Q1 2026 (using Irish MDD; it dropped by 0.2 per cent when using Irish GDP due to multinational activity), supported by consumption and investment, and broadly in line with previous quarters as the war in the Middle East only partially affected Q1. While expected to continue showing relative resilience in the face of current external shocks (partly reflecting a pickup in defence spending), challenges of relatively low productivity growth, increasing competitive pressures and strategic dependencies (including on imported fossil fuels), and an ageing population weigh on the longer-term growth prospects. The Chinese economy, which has been relatively insulated from the oil price shock to date given large stockpiles of oil, continued to expand, recording GDP growth of 5 per cent year-on-year in Q1. This growth however continues to be heavily dependent on international trade amid persistent weakness in domestic demand: while exports grew by 19.4 per cent year-on-year in May (imports grew 27.4 per cent but the trade surplus expanded), retail sales rose by a mere 0.2 per cent and house prices fell by 3.5 per cent annually in April, reflecting poor consumer confidence and stagnant demand.

Staff macroeconomic projections for the euro area (June 2026) were revised to reflect a stronger and more persistent than anticipated energy price shock. Eurosystem staff project euro area HICP inflation to average 3.0, 2.3, and 2.0 per cent in 2026, 2027 and 2028, respectively, representing significant upwards revisions for this year and next (by 0.4 and 0.3 per cent) due mainly to a higher path for energy prices. Real GDP growth forecasts over 2026 and 2027 were each trimmed by 0.1 per cent to 0.8 and 1.2 per cent, due to a stronger impact of the war on real incomes and confidence, while the 2028 forecast was slightly raised to 1.5 per cent. Uncertainty surrounding the baseline forecast remains very high, and risks remain tilted to the downside for growth and to the upside for inflation. In response to the inflationary pressures from the war in the Middle East, the ECB Governing Council decided in June to raise its three key interest rates by 25 basis points, bringing the deposit facility rate to 2.25 per cent. The Governing Council considers this move as robust across a range of scenarios mapping out how the shock might evolve and affect the medium-term outlook for the euro area. This leaves the Council well-positioned to navigate the current uncertainty generated by the war. The Governing Council will remain data-dependent in future decisions and is not pre-committing to any rate path.

Economic Activity

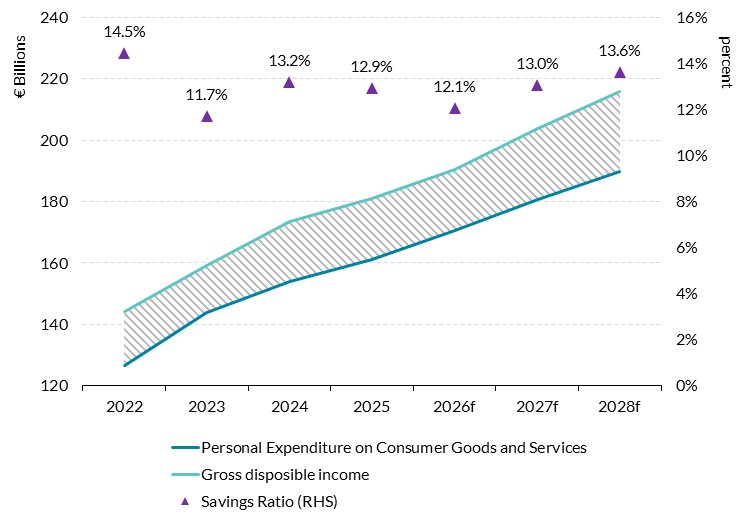

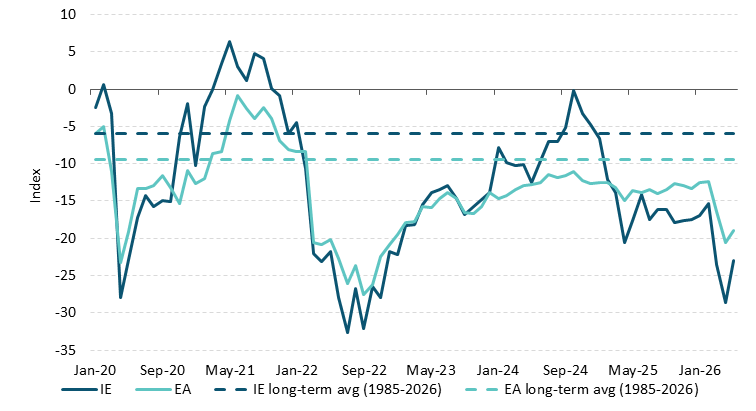

Despite strong outturns for the first quarter of the year, the forecast for consumption has been revised down from the projections in the previous Bulletin, largely due to higher-than-expected inflation lowering real income growth. Consumption is forecast to grow by 1.8 per cent in 2026 before increasing to 1.9 per cent in 2027 and 2.0 per cent 2028. This marks a small downward revision for 2026 from 1.9 per cent in the previous Bulletin. The downward revision stems from two mostly offsetting factors. On the one hand, higher inflation from energy prices is resulting in a decline in real household disposable income, and additional indicators point to a weaker labour market than previously forecast. On the other hand, 2026 Q1 consumption was strong, slightly above expectations from the previous Bulletin, though these were largely unaffected by the conflict in the Middle East which only began in March. High-frequency measures of consumption, which remained stable for the first quarter, have started showing some signs of weakening in April (Figure 11). The downward revision to consumption is less than the downward revision to employment and incomes, resulting in a lower savings rate relative to the previous Bulletin – now averaging 12.9 per cent from 2026 to 2028. Households are expected to temporarily save less to sustain consumption during the spike in energy prices. From 12.9 per cent in 2025, the savings ratio is forecast to fall to 12.1 per cent in 2026, before recovering to above 13 per cent as inflation normalises over the forecast horizon. Consumer confidence in Ireland has fallen over the last six months, from -17.5 in December to -28.6 in April before a slight pick up to -23 in May, in line with the euro area. Data from the ECB Consumer Expectations Survey (CES) showed a decline in expected incomes between February and April 2026, similarly observed in other euro area countries.

Savings rate expected to dip in 2026 as households deal with higher costs

Figure 9: Consumption, gross disposable income and the savings ratio (RHS)

Source: CSO and CBI calculations. Chart data in accessible format. (XLSX 164.97KB)

Consumer confidence had been declining in Ireland, with a small pick-up in May

Figure 10: Consumer confidence index for Ireland and the euro area

Source: European Commission and CBI calculations. Chart data in accessible format. (XLSX 164.97KB)

Latest observation May 2026.

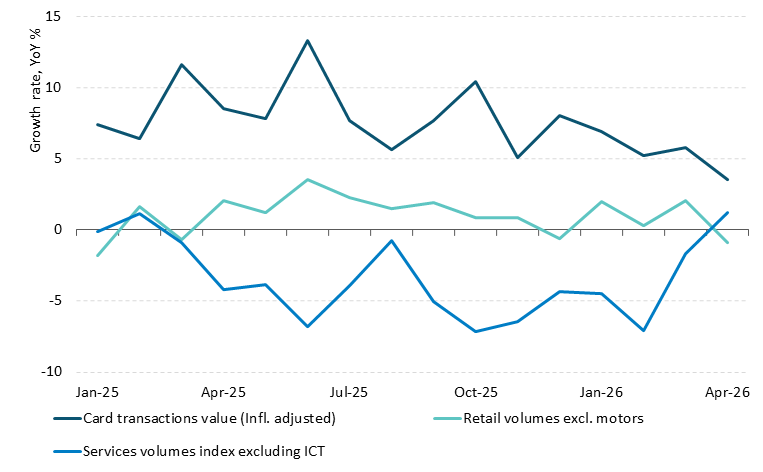

Higher frequency indicators of consumer spending were relatively stable for the first quarter of the year, but the April data showed signs of deterioration. The total value of card payments (in inflation-adjusted terms) has trended gradually downwards since mid-2025 but remained resilient up to and including March 2026, before falling slightly in April (Figure 11). Retail volumes remained relatively stable over the same period, before observing a similar decline in April, as a higher inflation rate may be showing early signs of affecting spending behaviour. In March and April, retail spending on fuels outpaced volumes significantly, consistent with rising energy prices. The monthly services turnover index (excluding ICT) fell over the course of 2025 but improved in consecutive months in March and April 2026 compared to the same months of the previous year. In summary, high-frequency consumption indicators indicate relatively resilient consumption so far in 2026, with a slightly negative turn in April for retail sales and card transactions. The impact of higher energy prices is expected to exert a continued downward pressure on consumption over the remainder of the year.

High-frequency consumption measures show some early signs of weakening in April 2026 after a strong start to the year

Figure 11: High frequency measures relating to consumer spending

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

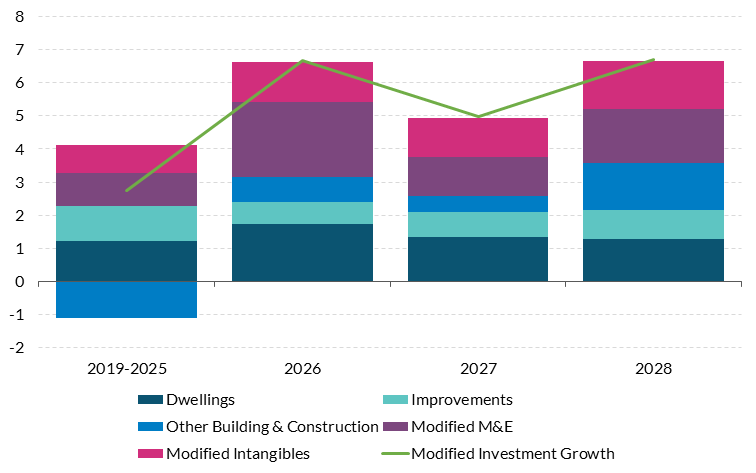

Modified investment is expected to continue building on the strong momentum experienced through 2025. Overall, forecasts for modified investment have been revised upwards from the previous Bulletin to an average of 6.1 per cent from 2026 to 2028 (Figure 12). This is largely due to recent outturns suggesting a substantial pickup in machinery and equipment (M&E) investment by multinational enterprises, led by significant increases in AI and data centre-related spending (see Box A). Despite significant uncertainty in the external environment, these multinational-dominated components of investment (machinery and equipment and modified intangibles) surprised on the upside in 2025 and have built further on this momentum so far in 2026. Imports of machinery and equipment increased by 45 per cent year-on-year in Q1 2026, driven by a substantial increase in office machines and data processing equipment (up 126 per cent year-on-year) and telecommunications equipment (up 68 per cent year-on-year). Modified M&E is forecast to grow by an average of 7.3 per cent over the forecast horizon. Following strong growth in 2025, modified intangibles are also forecast to increase by an average of 6.4 per cent over the same period. However, these components of modified investment are dependent on the activities of a small number of large foreign-owned firms and are therefore particularly (and potentially increasingly), volatile.

Modified investment growth is projected to be broad-based.

Figure 12

Y-o-Y Growth Contributions

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

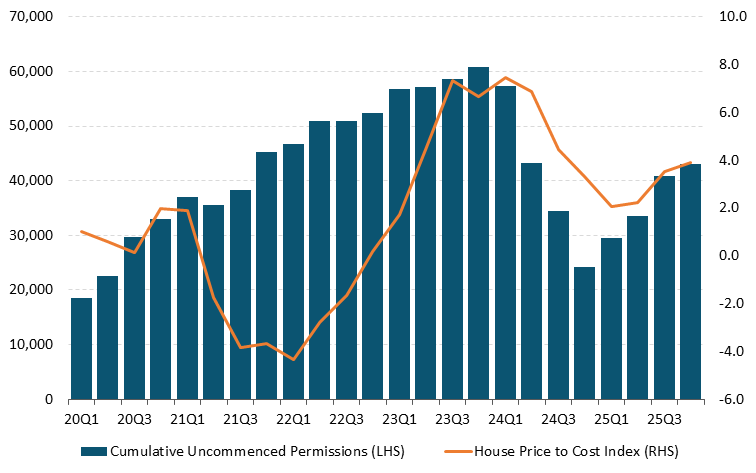

Projections of housing investment are in line with the previous Bulletin. With the Q1 2026 outturn coming in only marginally stronger than anticipated, housing completion forecasts remain unchanged at 40,000, 43,000 and 46,000 for 2026, 2027 and 2028, respectively. This is subject to improvements in dealing with infrastructural constraints referred to in previous Bulletins. The pool of uncommenced permissions grew throughout 2025 and currently stands at approximately 42,000. Continued improvements in viability as captured by the new house price to construction cost index (which increased by 3.7 per cent year-on-year in Q1 2026) suggest that an increasing portion of these uncommenced permissions might become viable (Figure 13). While the March 2026 Wholesale Price Index indicated only a slight acceleration in costs of 2.6 per cent year on year, the PMI input cost sub-index did rise substantially, indicating that producers are concerned about rising costs due to high energy prices. Commencements returned to 8,408 units in Q1 2026, following a period of volatility, with a surge in 2024 due to the expiry of energy and water connection waivers followed by very low levels throughout 2025. New home loans remain on an upward trend and increased by 15.1 per cent year-on-year in Q1 2026.

Uncommenced permissions provide a pool to draw from as viability improves

Figure 13

Annualised Units and Y-o-Y change

Chart data in accessible format. (XLSX 164.97KB)

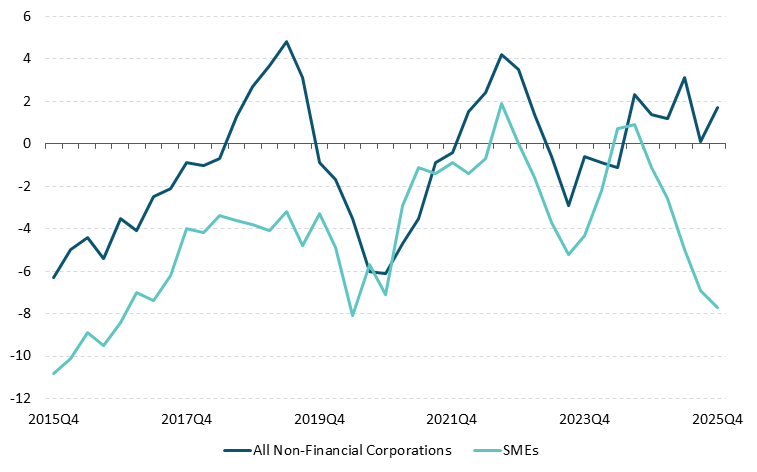

The divergence in bank lending to non-financial corporations and SMEs grew further in Q4 2025. The pace of growth in net lending by banks to Non-Financial Corporations (NFCs) increased in Q4 2025 to just 1.7 per cent year-on-year, while the decline in net lending to SMEs accelerated in Q4 2025, standing at 7.7 per cent year-on-year (Figure 14). Non-bank new lending to Irish enterprises was €938 million in Q3 2025, down from €972mn in Q3 2024. SMEs received new loans from non-banks worth €744 million in Q3 2025, while new loans to larger companies was significantly lower and stood at €193 million in the same quarter.

Growth in bank lending to SMEs continued to decline while increasing to larger firms

Figure 14

Y-o-Y growth

Source: Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

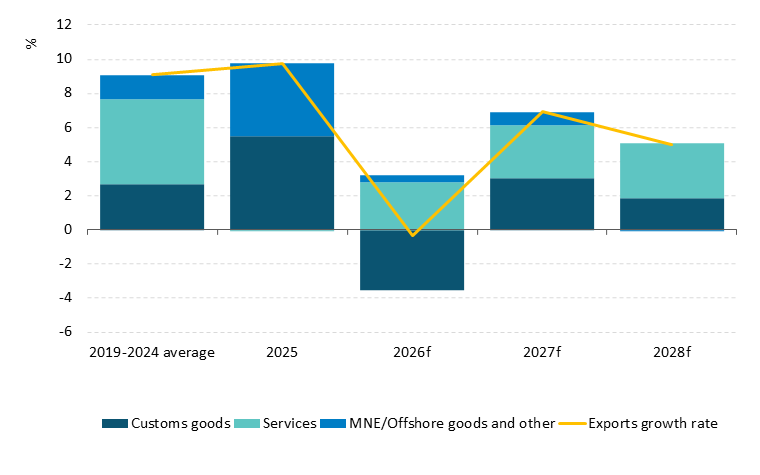

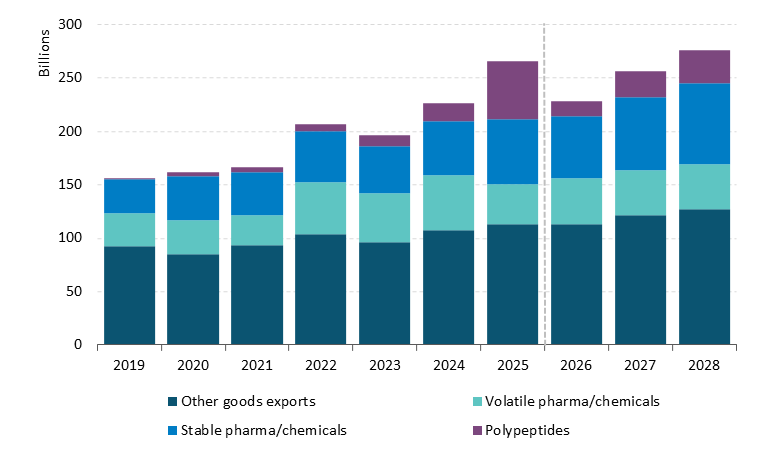

In line with the previous Bulletin, the pace of growth in overall exports is forecast to slow from 2026 to 2028, with growth in exports of services expected to be stronger than growth in goods. Real exports of goods and services are projected to fall by 0.3 per cent in 2026 before rebounding to 6.9 per cent in 2027 and 5 per cent in 2028 (Figure 15). As discussed in the previous Bulletin, the contraction in overall exports in 2026 reflects weakness in goods exports largely resulting from strong base effects from the 2025 polypeptide export surge (Figure 16). Last year saw an exceptional contribution of goods exports to headline trade. Real exports of goods and services rose by 9.7 per cent in 2025, with real goods exports up 23.5 per cent, while real services exports were broadly unchanged. Moreover, the swing in goods exports observed from Q1 2025 to Q1 2026 also reflects a decline in export unit-values, most notably for exports to the US (Figure 17). Customs trade detail show that the value of exports of polypeptide-hormones, which had surged to exceptional levels during 2025, remained at very low levels in Q1 2026, while other pharmaceutical and chemical exports remained stable on the previous quarter. In contrast, non-pharma customs exports grew to €31 billion in the quarter – exceeding both Q1 2025 and the 2025 quarterly average. As a result, the goods exports outlook for 2026 is not driven by weak external demand but rather by base effects from a strong 2025 combined with a weak 2026 first quarter of polypeptide hormone export values. Beyond 2026, both the pharmaceutical and non-pharmaceutical sub-components of customs good exports are expected to return to stable growth (Figure 16). Global demand for polypeptide-based pharmaceuticals appears solid over the medium-term, and additional production capacity in the pharma sector is due to be operationalised by late-2026. Services are expected to be the main source of exports growth over the forecast horizon, consistent with the 2019-2024 historical average. Real services exports are forecast to increase by 5.2 per cent in 2026, followed by growth of 5.5 per cent in 2027 and 5.8 per cent in 2028. Computer services remain a key driver, accounting for about 62 per cent of services exports in 2025. The offshore goods element of Irish trade can be large (as seen in 2025) but is also volatile and difficult to anticipate. Over longer durations its net contribution may be reduced due to offsetting positive and negative fluctuations. For these reasons the forecast use a mechanical rule – a moving average of the prior six quarters is applied over the forecast horizon.

Services exports expected to contribute most to overall export growth over the forecast horizon

Figure 15: Breakdown of annual real exports forecast over 2026-2028

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

All sub-component of goods exports are expected to continue growing from 2026, with a continued role for polypeptides

Figure 16: Customs goods exports, split by broad category

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Note: volatile pharma/chemicals mainly includes intermediate goods, whereas stable pharma/chemicals largely includes final retail/consumer goods and is observed to fluctuate less over time.

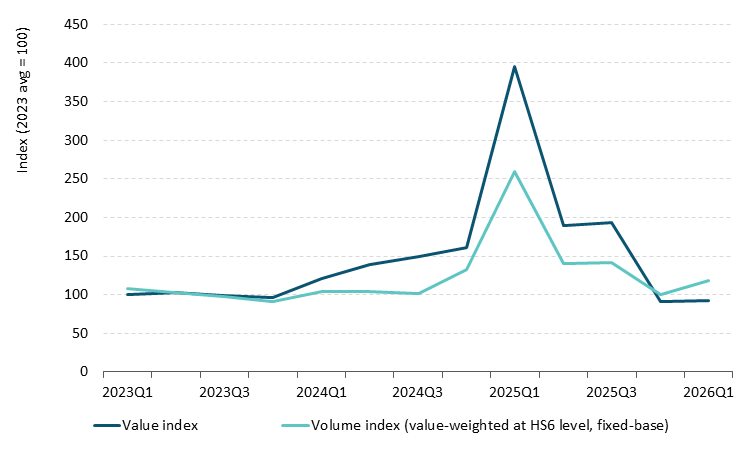

Large increase in unit values of goods exports in 2025 reversed in Q1 2026, most evident for Irish goods exports to the US

Figure 17: Value versus volume indices of IE goods exports to the US

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Note: The volume index is a value share-weighted aggregate of HS-6 level goods volumes with a fixed-2023 base.

Imports are expected to continue growing strongly, supported by demand for AI-related goods and imports of royalties/licenses. Real imports of goods and services are projected to grow by 3.8 per cent in 2026, 4.6 per cent in 2027 and 4.7 per cent in 2028. This is a significant revision upwards relative to the previous Bulletin in which import growth averaged 3.4 per cent over the forecast horizon. This increase is largely driven by stronger AI and data-centre related capital goods imports, in line with the upgraded outlook for modified investment and an expected continuation of strong growth in services imports of royalties/licenses. Box A provides detail on the rapidly growing contribution of AI and data-centre related imports to Irish trade. These include both capital goods used in data centres, which therefore enter modified investment and intermediate inputs used in production, which are in turn largely exported. New chip releases, as well as large-scale data centre stock replacement, may introduce greater volatility into Irish goods imports going forward. Higher prices for imported energy are also expected to increase the value of imports in 2026. As of Q1 2026, energy-related goods represented just 5.1 per cent of customs goods imports, a share that is expected to increase over the remainder of the year, but not to reach the highs of over 10 per cent experienced in Q1 2023.

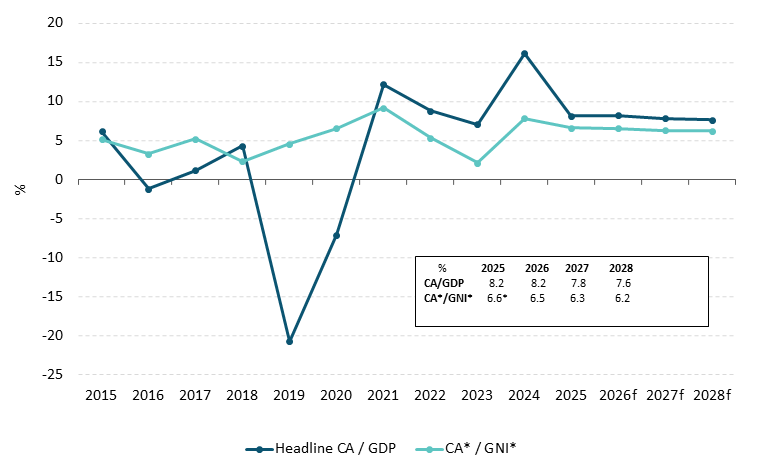

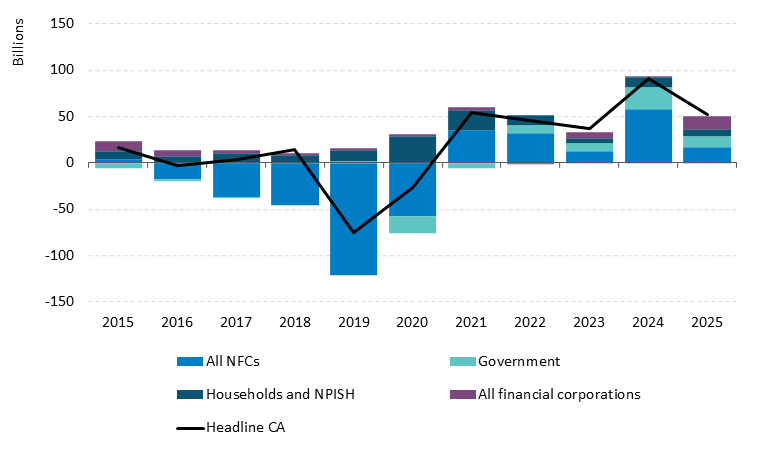

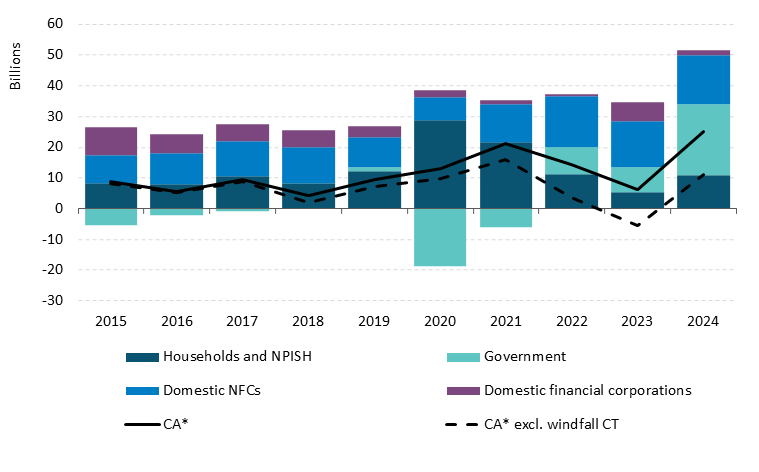

Ireland's external position is expected to remain in surplus over the forecast horizon. The modified current account (CA*), which adjusts the headline measure for distortions caused by globalisation-related flows of foreign-owned multinationals, is forecast to decrease from 7.8 per cent of GNI* in 2024 to 6.6 per cent in 2025 and to around 6.2 per cent through 2028 (Figure 18). The headline current account surplus contracted sharply from €91 billion (16.2 per cent of GDP) in 2024 to €52 billion (8.2 per cent of GDP) in 2025, despite the merchandise surplus widening from €176 billion to €230 billion. This decline was driven by primary income outflows related to foreign multinational profits, which expanded from €140 billion to €200 billion, whilst the services surplus narrowed from €60 billion to €26 billion. The headline surplus is forecast to remain at around 8 per cent of GDP, declining gradually over 2026 to 2028. A sectoral decomposition shows that the internationally dominated non-financial corporate sector accounts for most of the volatility in the headline current account, while the domestic private sector has consistently been a net lender over the last decade, contributing positively to the CA* surplus (Figure 20). As discussed in the previous Bulletin (Box B), enabling sustained higher investment could close the CA* surplus, for instance if housing output reached 55,000 units per annum and the domestic NFC investment rate approached the euro area average, the positive external balance for the domestic private-sector would be significantly reduced.

Headline and underlying external surpluses are forecast to remain sizeable

Figure 18: Headline current account/current account* as a share of GDP/GNI*

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Note: CA*/GNI* in 2025 is an estimate since these data are not released until July 2026.

Headline CA surplus dominated by activities of large multinational corporations (€bn)

Figure 19: Net lending/investment position of Irish resident sectors and headline CA

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Persistent excess saving by households and domestic businesses supports a positive CA* surplus (€bn)

Figure 20: Net lending/investment position of Irish domestic-only sectors and CA*

Source: CSO and Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Note: CA* data for 2025 will be released in early July.

Inflation

Headline HICP inflation forecasts have been revised upwards since the last Bulletin. HICP inflation is projected at 3.5 per cent in 2026 with forecasts of 2.9 per cent and 2.0 per cent for 2027 and 2028, respectively (Figure 8 and Table 2). The upward revisions are driven primarily by the sharp increase in energy prices in recent months (stemming almost entirely from liquid fuels, Figure 5) and the expectation that they will remain elevated for some time as reflected in higher technical energy price assumptions (Table 3 and Figure 6). These developments are broadly in line with the Adverse scenario presented in the March Bulletin’s Balance of Risks section. The energy price growth forecast for 2026 has been revised upward to 9.6 per cent, compared to the 6.4 per cent forecast in the previous Bulletin. Price increases for household gas and electricity have also recently been announced by a number of utility companies. Government fuel support measures, and the deferred carbon step and reductions in excise duty, somewhat temper the rise in energy prices and their contribution to headline inflation. Higher energy and input costs are expected to feed into food inflation which is forecast to rise to 3.8 per cent in 2027. Similar pressures feed into the prices of non-energy industrial goods components (NEIG), which in addition, have seen some recent positive momentum because of methodological revisions earlier this year (See Box D in the previous Bulletin). As a result, NEIG is estimated to make a small positive contribution to headline inflation in both 2026 and 2027. Recent month's data on services inflation are in line with expectations in the previous Bulletin, with services inflation averaging 3.4 per cent in the first quarter of 2026 (Figure 21). Measures of underlying inflation have remained below 3 per cent (Figure 22).

Table 2: Inflation Projections

| Indicator | 2025 | 2026 | 2027 | 2028 |

|---|

| HICP | 2.1 | 3.5 | 2.9 | 2.0 |

| Goods | 1.0 | 3.1 | 2.2 | 0.5 |

| Energy | -0.3 | 9.6 | 2.2 | -0.3 |

| Food | 3.7 | 2.2 | 3.8 | 2.1 |

| Non-Energy Industrial Goods | -0.4 | 1.1 | 1.0 | -0.3 |

| Services | 3.0 | 3.7 | 3.4 | 3.4 |

| HICP ex Energy | 2.3 | 2.9 | 2.9 | 2.3 |

| HICP ex Food & Energy (Core) | 2.0 | 3.0 | 2.8 | 2.3 |

Source: CSO, Central Bank of Ireland

There have been further upward revisions to technical assumptions underlying the inflation forecasts since the previous Bulletin. The most significant upward revision has been to oil prices, up 30.6 per cent per cent for 2026, compared to the last Bulletin. The Synthetic Energy commodity price index is revised up by 23.1 per cent, while wholesale electricity and gas prices were revised by 9.7 per cent and 8.4 per cent respectively. Food price assumptions from the European Commission, use-weighted, remain broadly aligned with the previous Bulletin. The euro exchange rate assumptions with respect to the USD and GBP are also mostly in line. Non-energy commodities have seen a further revision upward of approximately 4.6 per cent for 2026.

Table 3: Changes in key technical assumptions

| Indicator | QB2 2026 | QB1 2026 |

|---|

| 2025 | 2026 | 2027 | 2028 | 2025 | 2026 | 2027 | 2028 |

|---|

| Oil (USD/barrel) | 69.13 | 96.59 | 82.23 | 77.12 | 69.13 | 74.16 | 67.98 | 66.72 |

| Natural gas (EUR/MWh) | 36.25 | 45.62 | 37.51 | 27.87 | 36.25 | 42.09 | 30.53 | 23.57 |

| Wholesale electricity (EUR/MWh) | 83.63 | 89.30 | 78.19 | 68.06 | 83.63 | 81.40 | 71.55 | 64.17 |

| Non-energy commodities (USD, per cent change*) | 5.80 | 3.02 | 0.85 | -1.94 | 5.82 | -1.53 | 0.75 | -0.14 |

| EUR/USD | 1.13 | 1.17 | 1.17 | 1.17 | 1.13 | 1.17 | 1.17 | 1.17 |

| EUR/GBP | 0.86 | 0.87 | 0.87 | 0.87 | 0.86 | 0.87 | 0.87 | 0.87 |

Source: ECB, Refinitiv. Notes: *Annual per cent change. Cut-off date: May 22nd, 2026

Services inflation remaining steady during start of 2026

Figure 21: Contributions to services inflation

Year-on-year per cent change (%)

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

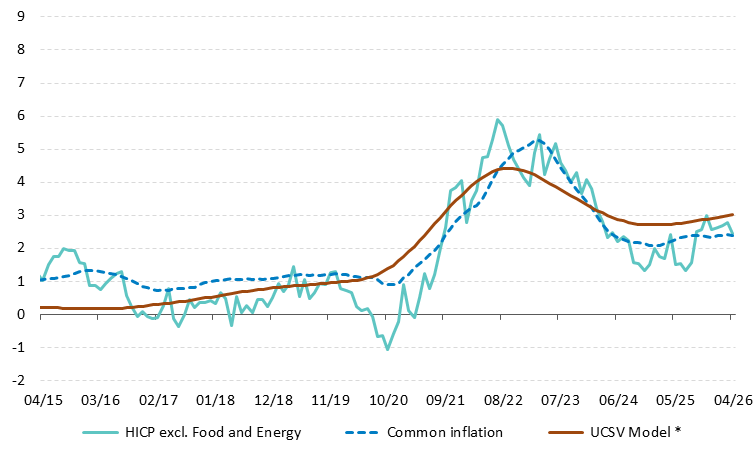

Marginal increase in underlying inflation measures without evident structural momentum

Figure 22: Underlying measures of inflation

Year-on-year per cent change

Source: Eurostat, Central Bank of Ireland calculations. Chart data in accessible format. (XLSX 164.97KB)

Note: UCSV Model stands for unobserved components model with stochastic volatility.

Labour Market and Earnings

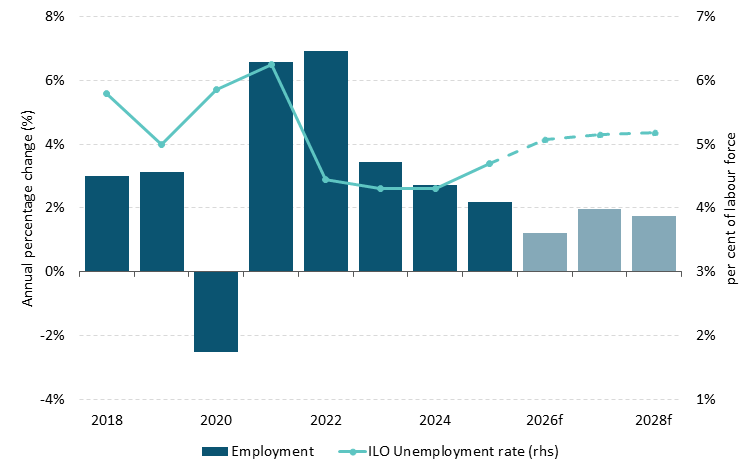

The outlook for employment growth has weakened since the last Bulletin against a more uncertain background with divergence across indicators. With a weak outturn in Q1 reported in the Labour Force Survey, annual employment growth in 2026 is being revised down to 1.2 per cent. However, other labour market indicators point to stronger growth consistent with a normalisation rather than a persistent slowdown. Employment growth is projected to increase by 2 per cent in 2027 influenced by favourable base effects, before easing to 1.8 per cent in 2028 (Figure 23). The annual average unemployment rate is forecast to increase to 5.1 per cent in 2026 and gradually rise to 5.2 per cent in 2028. Against this background, real wage growth is expected to average 0.6 per cent over the forecast horizon though more persistent inflationary developments present downside risks.

Employment levels from the Labour Force Survey were relatively unchanged in Q1 2026 compared to a year earlier, though other labour market indicators suggest steady growth. The year-on-year change in employment in Q1 2026 was flat, while employment contracted on a seasonally adjusted quarterly basis by 0.6 per cent. Outside of the pandemic period, this year-on-year growth rate is the lowest observed since 2012. At a sectoral level, employment losses were observed in 8 of the 14 sectors, the largest of which were in the Admin (-10.7 per cent) and ICT sectors (-10.6 per cent). Employment levels in the ICT sector are likely to be adversely affected by the recent announcement of job cuts in Q2, though general demand for workers with digital skills across the economy may limit the impact on unemployment figures (See Box B for further information on the role of MNEs in the labour market).

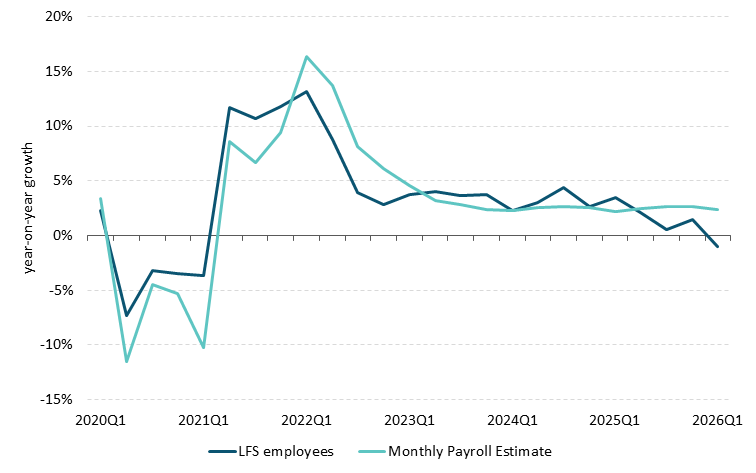

The LFS remains the principal measure of employment in Ireland; however, as a quarterly survey, short-term movements can be influenced by factors such as sampling variability. This is particularly relevant when trends in survey-based data diverge from administrative data such as the CSO monthly employee payroll data which exhibited average year-on-year growth of 2.4 per cent in Q1. Growth rates in employee levels in the LFS and monthly payrolls have diverged since mid-2025, with payroll data pointing to stronger labour market conditions. However, there are fundamental differences between the two measures in scope and in terms of how they are measured (Figure 24). Broader indicators of labour market activity also point to stronger conditions with cumulative employment permits for the year to May up 15.3 per cent compared to 2025 and cumulative income tax receipts 7.5 per cent higher in nominal terms over the same period. Positive employment developments are expected for the remainder of the year resulting in annual growth of 1.2 per cent for 2026 as a whole, though a continued divergence between survey and administrative data presents a significant downside risk to the forecast.

Employment growth forecast to remain positive, while the unemployment rate rises marginally above 5 per cent

Figure 23: Employment and unemployment forecast profiles

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

Measures of employee headcount have diverged of late

Figure 24: Year-on-year growth in employee levels

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

Note: The LFS measures the number of persons in employment and the monthly payroll records the number of employments. Levels may differ due to persons with multiple employments or the timing of when the LFS respondents are surveyed within the quarter.

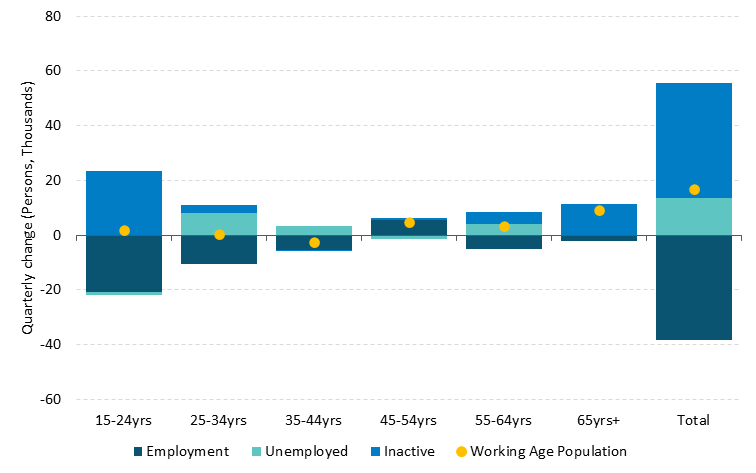

The unemployment rate has increased over the past year with forecasted rates above 5 per cent for the first time since 2021. The seasonally-adjusted ILO unemployment rate in Q1 2026 measured 5 per cent, up from 4.6 per cent in Q4 2025 and the highest level since Q4 2021. This increase would have been larger if not for a decline in labour force participation amongst 15-24 year olds as those leaving employment moved out of the labour force rather than into unemployment (Figure 25). This pattern is consistent with seasonal fluctuations in youth labour market activity as participation rates typically peak in Q2 and Q3 as younger cohorts seek summer employment. These movements are expected to add to aggregate employment growth in 2026.

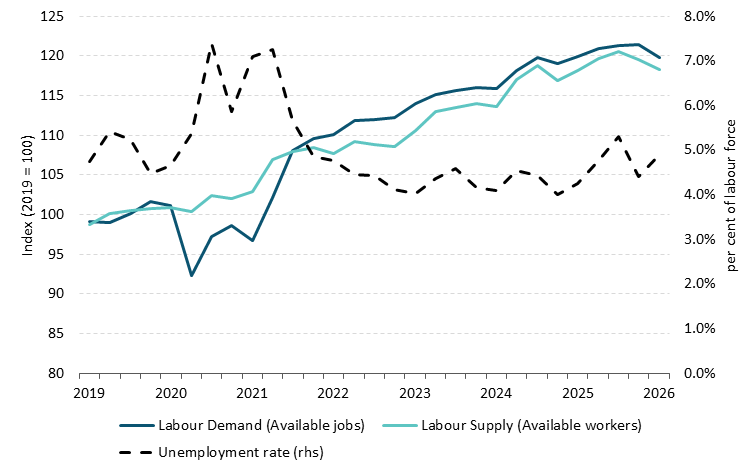

Various indicators show signs of a continued slowdown in labour demand. Indeed job postings are down 8.9 per cent year-on-year in May 2026 and now below the pre-pandemic level. Data from CSO EHECS indicates that the job vacancy rate has eased to 1.1 per cent in Q1 2026 though remains above its long-run average of 0.9 per cent from 2008 onwards. Taken together, labour demand (the number of available jobs) continues to grow at a faster rate than labour supply (the number of available workers) which has helped to explain the relative stability of the unemployment rate in recent years (Figure 26). Further deterioration in labour demand conditions alongside an increasing population size of younger age cohorts could see higher unemployment rates as workers face difficulties accessing employment (as outlined in Box E of QB1 2026). The unemployment rate is projected to average 5.1 per cent in 2026 and gradually increase thereafter to 5.2 per cent in 2028.

The recent rise in inactivity is driven by younger-age cohorts

Figure 25: Quarter-on-quarter change in labour market status (Q1 2026)

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

Labour slack is slowly increasing as labour demand moderates

Figure 26: Job postings and seasonally-adjusted monthly unemployment rate

Source: CSO. Chart data in accessible format. (XLSX 164.97KB)

Note: Labour demand is the sum of the employment level and job vacancies. Labour supply is the sum of the labour force and the potential additional labour force.

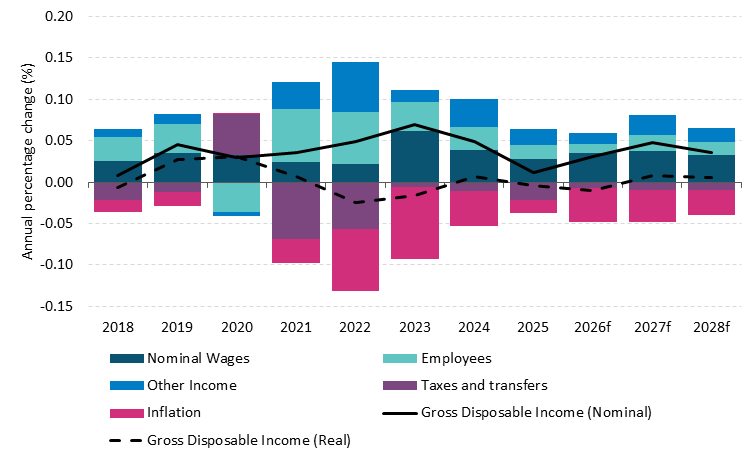

Nominal wage growth forecasts may be affected by future revisions to historical data, though positive real growth is projected over the forecast horizon. Nominal compensation per employee (CPE) increased by 3.1 per cent in 2025, equivalent to 1.6 per cent in real terms. However, growth is expected to be revised upwards in the forthcoming Annual National Accounts release once additional data are included (See Figure 21 of QB1 2026). Despite this uncertainty, CPE is projected to increase in nominal terms by 4 per cent and 4.1 per cent, respectively in 2026 and 2027. Growth is then projected to slow to 3.7 per cent in 2028 as labour market conditions ease and unemployment rises modestly. Real Gross Disposable Income per household is forecast to decline by 1 per cent in real terms in 2026 due to elevated inflation and increase by an annual average of 0.7 per cent in 2027 and 2028, respectively (Figure 27). There are a number of upside and downside risks to the wage projections as the continued slowdown in job postings alongside redundancy announcements in the higher-paying ICT sector may exert downward pressure on nominal wage growth this year. At the same time, uncertainty remains regarding the next public sector pay agreement with the current deal due to expire in June 2026.

Decline in real gross disposable income in 2026 followed by pick up in 2027 and 2028

Figure 27: Year-on year growth in gross disposable income per household and underlying components (per cent)

Source: CSO and author’s calculations. Chart data in accessible format. (XLSX 164.97KB)

Table 4: Labour Market Forecasts

| Indicator | 2024 | 2025 | 2026f | 2027f | 2028f |

|---|

| Employment (000s) | 2,757 | 2,818 | 2,852 | 2,908 | 2,959 |

| % change | 2.7 | 2.2 | 1.2 | 2.0 | 1.8 |

| Labour Force (000s) | 2,880 | 2,955 | 3,004 | 3,066 | 3,121 |

| % change | 2.7 | 2.6 | 1.7 | 2.1 | 1.8 |

| Participation Rate (% of Working Age Population) | 65.8 | 66.1 | 66.0 | 66.2 | 66.2 |

| Unemployment (000s) | 123 | 137 | 152 | 158 | 162 |

| Unemployment (% of Labour Force) | 4.3 | 4.7 | 5.1 | 5.2 | 5.2 |

Public Finances

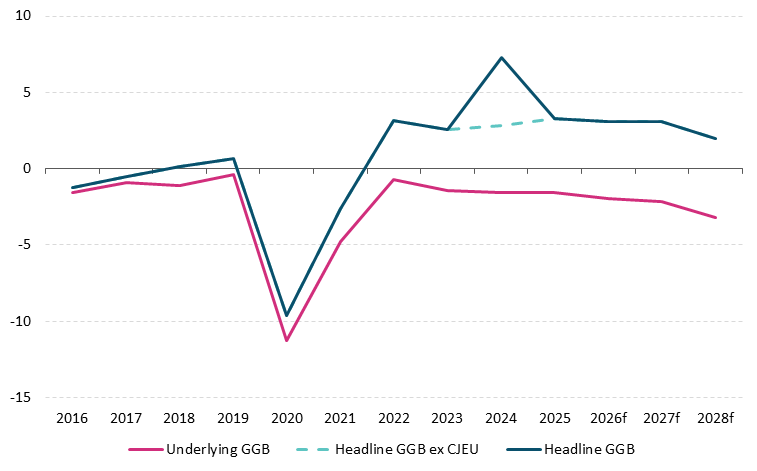

The underlying budget deficit, which excludes windfall corporation tax (CT) receipts, is projected to worsen over the forecast horizon as expenditure growth is expected to exceed that of revenue growth. Annual underlying revenue is projected to grow by 5.8 per cent on average over the 2026-2028 period, while average annual spending growth is expected to rise by 7.4 per cent. As a result, the underlying budget deficit is projected to more than double from 1.5 per cent of GNI* in 2025 to 3.2 per cent in 2028 (Table 5). These projections are more favourable than at the time of the March Quarterly Bulletin, partly reflecting a stronger outturn for 2025 than had been anticipated at that time. A headline general government (GG) surplus of €11.2bn was recorded in 2025 (estimated at 3.3 per cent of GNI*), with the better outturn primarily due to expenditure being lower than what had been expected at the time of Budget 2026. Looking ahead, the headline budget balance is forecast to remain in surplus, driven by strong CT growth, which is expected to benefit from the implementation of the Minimum Tax Directive in 2026 and 2027. Nevertheless, the headline surplus is still forecast to decline over the forecast horizon to 2 per cent of GNI* in 2028 (Figure 28), reflecting the deterioration in the underlying budgetary position. A Signed Article (PDF 1.01MB) accompanying this Bulletin assesses the medium-term outlook for the public finances.

Table 5: Key Fiscal Indicators, 2025-2028

| Indicator | 2025 | 2026(f) | 2027(f) | 2028(f) |

|---|

| GG Balance (€bn) | 11.2 | 11.4 | 12.1 | 8.4 |

| GG Balance (% GNI*) | 3.3 | 3.1 | 3.1 | 2.0 |

| GG Balance (% GDP) | 1.8 | 1.7 | 1.7 | 1.1 |

| GG Debt (€bn) | 209.9 | 206.2 | 205.1 | 209.9 |

| GG Debt (% GNI*) | 61.4 | 56.0 | 52.4 | 50.2 |

| GG Debt (% GDP) | 32.9 | 31.4 | 28.8 | 27.8 |

| Estimated Windfall CT (€bn) | 16.5 | 18.7 | 20.5 | 21.8 |

| Underlying GGB (€bn) | -5.2 | -7.3 | -8.4 | -13.4 |

| Underlying GGB (% GNI*) | -1.5 | -2.0 | -2.1 | -3.2 |

Source: Central Bank of Ireland Projections

Note: Underlying GGB excludes estimates of excess CT and receipts from the Apple state aid case; (e) is for estimate; (f) is forecast

Underlying GG deficit is projected to deteriorate over the forecast horizon, particularly in 2028

Figure 28: per cent of GNI*

Source: CSO, Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Note: Underlying GGB excludes Central Bank estimates of excess corporation tax receipts and receipts from Apple State aid case; CJEU is Court of Justice of EU ruling on Apple state aid case.

The projected strong growth in government expenditure in the coming years is expected to be relatively broadly based. The Government’s Annual Progress Report 2026 (APR 2026), which was published in April, provided updated medium-term expenditure forecasts. This included revised forecasts for net primary spending. It is now expected to grow by 7.4 per cent this year, up from 6.6 per cent in the Medium-Term Fiscal and Structural Plan, published just four months earlier. Both current and capital spending are projected to record large increases in the coming years, with the latter expected to reach 6 per cent of GNI* in 2028, close to double its level of a decade earlier. Strong tax revenue growth occurred in the first five months of the year, with receipts up 6.1 per cent year-on-year when revenue linked to the Apple state aid case is excluded. CT receipts are projected to contribute significantly to overall revenue growth in the coming years, although there remains uncertainty over the exact impact of the Minimum Tax Directive and the effect of US trade and tax policy. Additionally, in response to the US-Iran conflict, the Government implemented fiscal supports, mostly on the revenue side, which are estimated to cost €755mn. These measures are due to expire by the end of July. The factors that pose a risk to the public finances are discussed in further detail in the Balance of Risks below.

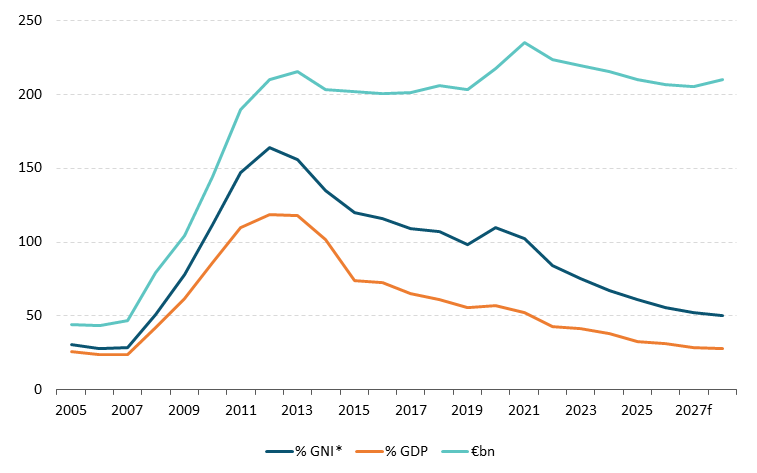

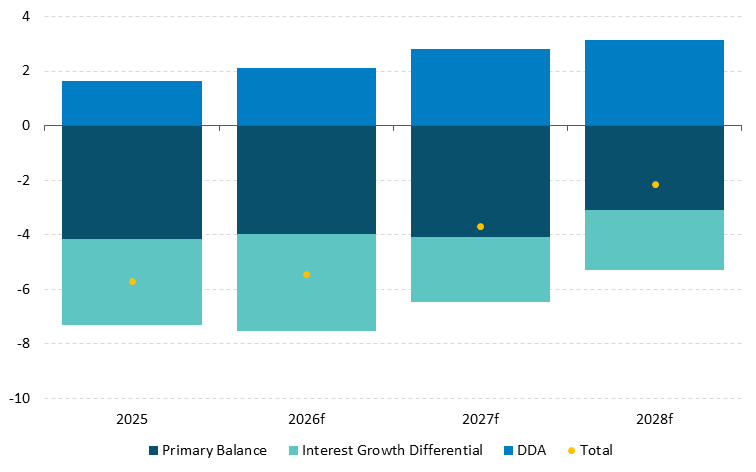

The General Government debt (GGD)-to-GNI* ratio is projected to continue to decline over the medium term. The debt ratio is expected to fall from 61.4 per cent of GNI* in 2025 to 50.2 per cent in 2028 (Figure 29). This reflects a combination of projected headline primary surpluses (averaging 3.7 per cent of GNI* over 2026-2028) and the expectation of a continuing favourable interest rate-growth rate differential (Figure 30). The supportive impact of the latter is expected to weaken, however, against the backdrop of a tightening of financing conditions. The State’s annual interest costs are forecast to double from €3bn in 2025 to €6bn in 2030, with the effective interest rate also expected to double to around 3 per cent over the same period. The National Treasury Management Agency (NTMA) has so far this year raised €8.25bn through bonds sales, roughly 70 per cent of its funding range for the year. Ireland’s cash position remains strong, with a liquid balance (inclusive of receipts from the Apple state aid case) of €21.7bn at end-May. Part of these balances were used to redeem the €12bn treasury bond that expired in May.

Debt ratio is projected to fall to close to 50 per cent of GNI* by the end of the forecast horizon

Figure 29: per cent of GNI*, per cent of GDP*, €billion

Source: CSO, Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Projected headline budget surpluses and nominal growth are supporting a continued fall in the public debt ratio out to 2028, but interest rate on debt is rising

Figure 30: per cent of GNI*

Source: Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Notes: I-G Differential is interest rate-growth rate differential; DDA is the deficit-debt adjustment

Balance of Risks to the Outlook

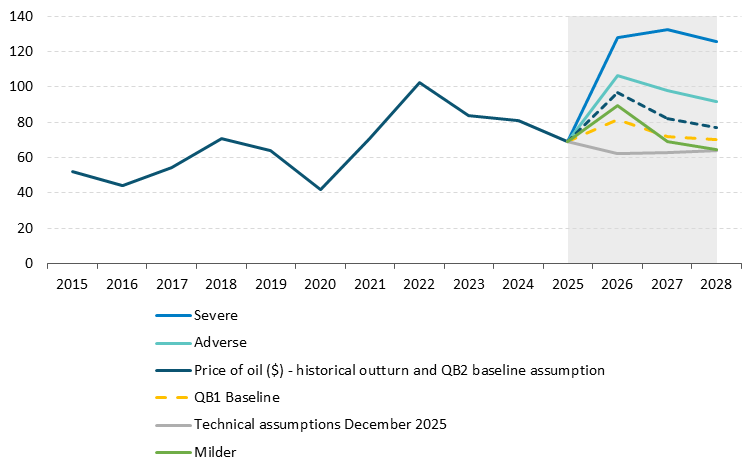

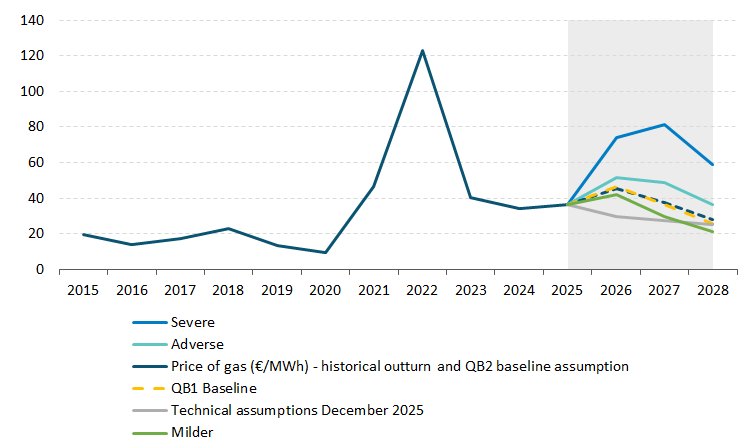

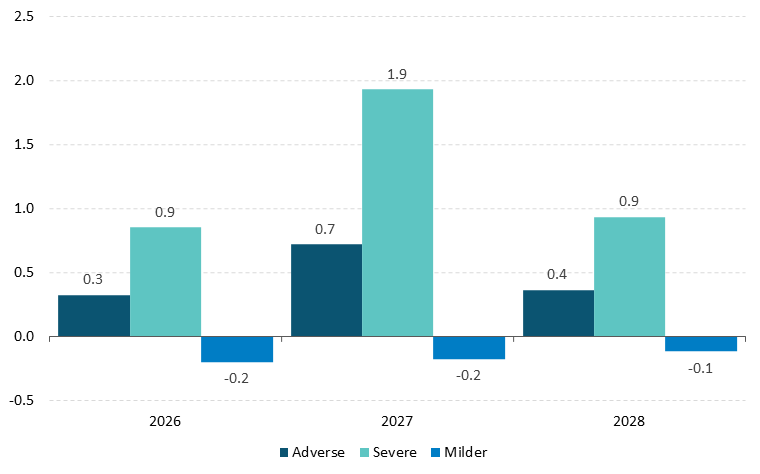

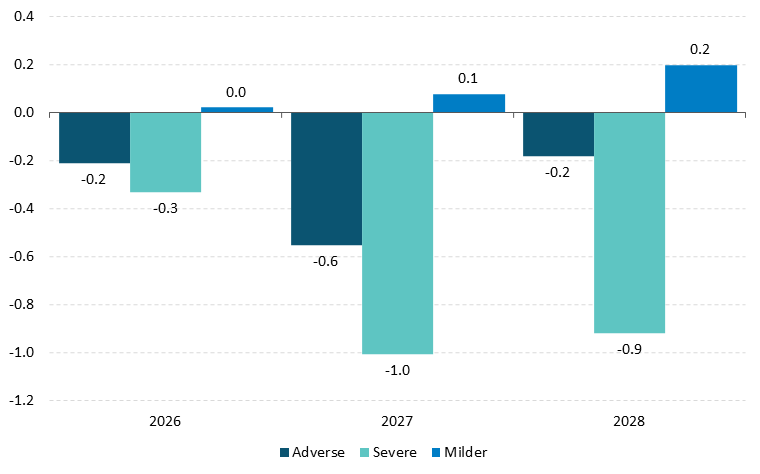

The balance of risks to the overall outlook for economic activity is firmly tilted to the downside, with inflation risks clearly to the upside. The central forecasts incorporate higher energy price assumptions compared to those which underpinned the previous projection in March 2026. The latter had already been revised up compared to the energy price paths from December 2025, before the outbreak of the war in the Middle East (Figure 31 and Figure 32). On 15 June 2026, the US and Iran announced a memorandum of understanding to extend their ceasefire by 60 days and reopen the Strait of Hormuz. The agreement is due to be signed on Friday 19 June. At the time of writing, there remains uncertainty as to when the current disruption to the Strait of Hormuz shipping lanes – vital for the transportation of oil and gas from the Persian Gulf – is likely to be alleviated and the extent to which trade through the Strait normalises. Depending on the course the conflict takes and the durability of the new agreement, there is a risk that energy prices could be higher than assumed in the central forecasts, while a more benign outcome is also possible. Given this uncertainty, alternative stylised scenarios are presented as in our previous Quarterly Bulletin in March 2026. In the milder scenario, oil and gas prices are around 15-20 per cent below the baseline levels throughout the horizon. This projected path may arise should the conflict be resolved swiftly, leading to a rapid normalisation of global oil and gas markets. In contrast, the adverse and severe scenarios assume higher energy price and food commodity prices, heightened uncertainty and tighter credit conditions. In the adverse scenario, global oil and gas prices rise by 10 and 14 per cent, respectively, above the baseline in 2026, with prices remaining persistently higher than the baseline out to the end of 2028. The adverse scenario also assumes that global food prices rise by 12 per cent by end 2028. In the severe scenario, the equivalent increases in oil and gas prices in 2026 are 32 and 63 per cent, respectively. In this scenario energy prices remain persistently elevated out to 2028 (Figure 31 and Figure 32) with some amelioration in the price level in 2028 which is, in part, a reflection of the profile of the baseline. The severe scenario assumes that global food prices rise by 24 per cent by end 2028. One of the main differences between the updated scenario assumptions compared to those used in our previous Quarterly Bulletin is that energy prices in the adverse scenario no longer return to the baseline in 2027 but remain higher across the whole projection period. The increase in energy prices in the severe scenario is also assumed to be more persistent.

Higher energy and food commodity prices relative to baseline assumptions would increase inflation and reduce growth in Ireland relative to the central forecast. In the adverse scenario, inflation would increase by 0.3 percentage points and MDD growth would be 0.2 percentage points lower in 2026 than in the baseline (Figure 33 and Figure 34). In the severe scenario, involving more significant and persistent increases in energy and food prices, inflation would be 0.9 percentage points higher in 2026 and MDD growth would be 0.3 percentage points lower than in the baseline projections. In the updated severe scenario, an estimated further 1.9 percentage points would be added to inflation in 2027, with MDD growth 1 percentage point lower. Applying these estimated impacts from the severe scenario to the central forecasts, HICP inflation would stand at 4.4 per cent and 4.8 per cent in 2026 and 2027 respectively. MDD growth would be reduced to 3 per cent in 2026 and 1.8 per cent in 2027. Higher global commodity prices would reduce economic activity in Ireland’s main trading partners, thereby lowering external demand for the traded sector of the economy. This results in a decline in exports and activity this sector which, over time, spills over to investment and the broader domestic economy, further reducing MDD and contributing to a decline in overall output, relative to the baseline projection. In the milder scenario, international energy prices decline more swiftly reducing the pressure on inflation. This would benefit economic activity in Ireland and support stronger global growth. Inflation in Ireland would be slightly lower than in the baseline across the forecast horizon, but would still remain above the rates projected before the conflict as the impact of the large rise in energy prices already experienced takes time to recede.

Updated scenario assumptions related to the Middle East conflict

Figure 31: Oil prices (level), $ per barrel

Source: ECB. Chart data in accessible format. (XLSX 164.97KB)

Figure 32: Gas prices (level), € per MWh

Source: ECB. Chart data in accessible format. (XLSX 164.97KB)

Swift resolution of Middle East war would benefit the economy but escalation would see higher inflation and weaker growth than in the baseline

Figure 33: Inflation, p.p. deviation from baseline

Source: Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

Figure 34: MDD growth, p.p. deviation from baseline

Source: Central Bank of Ireland. Chart data in accessible format. (XLSX 164.97KB)

These scenarios are partial and likely underestimate the impact on growth and inflation of any further surges in energy prices. The scenarios provide estimates of the sensitivity of baseline inflation and growth forecasts to a change in key conditioning assumptions but there are caveats that should be considered in interpreting the results. First, a sharper increase in energy prices than those considered in the severe scenario, while unlikely, could occur if inventories fall dramatically and supply from other regions outside the Middle East does not sufficiently fill the gap to meet global demand. Even so, the scenarios consider the impact of increases in energy and food commodity prices along with higher uncertainty a tightening of financing conditions. An escalation of the conflict could trigger more complex risks to global supply chains for a broader range of commodities and these effects are not explicitly included or may not be adequately captured in the scenarios (see Box C). These indirect effects from elevated energy costs could see larger impacts on inflation and growth than reported here. If combined with more pronounced second-round effects arising from wage adjustments, these could provide further upward pressures to prices and increase the persistence of this shock on headline inflation. As is the standard convention, the scenarios assume monetary and fiscal policy are unchanged compared with the baseline.

The balance of risks to the export forecast is to the downside given the high level of concentration in pharma and ICT exports, amidst continued risk of shifts to international trade and investment policies. The baseline forecasts assume a recovery in polypeptide hormone exports over the remainder of 2026 from their low levels at the beginning of the year. A more persistent fall back in polypeptide hormone exports than projected in the baseline would materially lower headline exports and GDP, given the outsized contribution of this product category to Irish exports. On the upside, if global demand for diabetes and obesity treatments continues to rise rapidly, pharma exports could remain higher for longer than assumed in the baseline. There is considerable uncertainty around our baseline projections for the path of goods exports, particularly in light of a recent divergence between volume-based measures of exports to the US and the value assigned to these (Figure 17). Services exports could outperform if higher global investment in ICT and AI translates into stronger exports of computer and business services from Ireland and if the adoption of AI technologies yields productivity improvements. This could also result in higher domestic investment than in the baseline forecasts. Over the medium term, there are downside risks to Irish exports and corporation tax receipts if US companies actively reduce the volume and value of their activity in Ireland. Changes in US corporate tax or industrial policy could affect the location of intangible assets and production, with knock on effects for goods and services trade, investment and corporation tax receipts. Firms in the services sector differ from their counterparts in the manufacturing sector as the required sunk investments in Ireland tend to be lower. As a result, the activity and employment arising from the MNE-dominated parts of the services sector is likely to be more sensitive to negative shocks.

AI-related developments are likely to have a meaningful impact on the economy over both the short and medium term, though both the magnitude and nature of these changes are highly uncertain. As discussed in Box A, AI-related trade and investments are growing rapidly and are likely to add volatility to modified investment and goods imports. The rapid recent developments in artificial intelligence have increased private investment in several multinational ICT companies with operations in Ireland, with positive implications for the Irish economy. However, there are potential downside risks. The frontier of AI development is taking place in a small number of foreign companies. Their market valuations are dependent on exceptional future earnings, and a continued pace of improvement in the underlying technologies they are developing. Despite their huge potential, any adverse developments in their business models or disappointments in the trajectory of their products may lead to a correction in equity prices for the broader technology sector with implications for Ireland, including lower exports, investment, employment and tax revenue. However, this same exposure presents upside risk. Over the medium term, there is a lot of uncertainty around the purported productivity impact of AI, and how this will reshape the labour market. In principle, AI-related productivity increases could boost growth, both directly through adoption by Irish-based firms, and indirectly through Ireland’s substantial trade and investment links to the U.S. and the rest of the world. In terms of FDI, almost 6-7 per cent of business employment is in IDA-supported services firms, which are largely U.S. technology-related (see Ruane et al., 2025 (PDF 1.4MB)). These firms are likely to be early adopters of AI, presenting a double-sided risk. On the one hand, they may see their labour share drop as AI substitutes for an increasing number of tasks. On the other hand, this may enable them to gain global market share and increase scale. The net effect on employment is ambiguous. In addition, a new generation of U.S. technology firms are growing amidst the AI revolution. Whether Ireland can continue the role it has played historically as the European headquarters of U.S. tech multinationals will play an important role in shaping future FDI, employment and tax revenue. More broadly, Yadav and McIndoe Calder (2026) (PDF 1.8MB) show that a substantial proportion of workers in the Irish labour market are in occupations with some exposure to AI, albeit with differing degrees of complementarity. Whether the productivity gains from AI are achieved by complementing workers or substituting for them will determine the overall impact on employment and wages.

There is a risk that capacity constraints could become worse if progress on alleviating infrastructure gaps in the economy is delayed or inadequate. This risk could arise even if a slowdown in the pace of economic growth transpires. Planned expenditure under the National Development Plan is designed to address shortages of critical infrastructure in water and waste water, energy, transport and housing. Reforms such as those in the Accelerating Infrastructure Report and Action Plan are designed to reduce delays in the delivery of large national infrastructure projects. Delayed progress resulting in persistent deficits in basic infrastructure represent a downside risk to the projections for investment. If this materialised, lower investment would act as a drag on long-term growth and productivity. Over the short run, this could result in higher and more persistent inflation triggered by domestic pressures and, with competitiveness impaired, weaker economic growth occurring over the longer term. Domestic capacity constraints and inflationary pressures – and the associated negative implications for long-term growth – would be aggravated if the pattern of procyclical budgetary policy persists.

Detailed Forecast Table

| | 2024 | 2025e | 2026f | 2027f | 2028f |

|---|

Constant Prices | | | | | |

| Modified Domestic Demand | 1.8 | 4.9 | 3.3 | 2.8 | 3.3 |

| Modified Gross National Income (GNI*) | 4.8 | 4.7 | 2.4 | 3.0 | 3.5 |

| Gross Domestic Product | 2.6 | 12.3 | -2.7 | 6.5 | 4.0 |

| Final Consumer Expenditure | 3.0 | 2.9 | 1.8 | 1.9 | 2.0 |

| Public Consumption | 4.8 | 3.9 | 3.4 | 2.8 | 2.8 |

| Gross Fixed Capital Formation | -28.5 | 42.6 | 3.5 | 3.0 | 3.9 |

| Modified Gross Fixed Capital Formation | -4.2 | 10.9 | 6.7 | 5.0 | 6.7 |

| Exports of Goods and Services | 8.6 | 9.7 | -0.3 | 6.9 | 5.0 |

| Imports of Goods and Services | 2.7 | 9.5 | 3.8 | 4.6 | 4.7 |

| Total Employment | 2.7 | 2.2 | 1.2 | 2.0 | 1.8 |

| Unemployment Rate | 4.3 | 4.7 | 5.1 | 5.2 | 5.2 |

| Harmonised Index of Consumer Prices (HICP) | 1.3 | 2.1 | 3.5 | 2.9 | 2.0 |

| HICP Excluding Food and Energy (Core HICP) | 2.3 | 2.0 | 3.0 | 2.8 | 2.3 |

| Compensation per Employee | 4.3 | 3.1 | 4.0 | 4.1 | 3.7 |

| General Government Balance (% of GNI*) | 7.3 | 3.3 | 3.1 | 3.1 | 2.0 |

| ‘Underlying’ General Government Balance (% of GNI*) | -1.6 | -1.5 | -2.0 | -2.1 | -3.2 |

| General Government Gross Debt (% of GNI*) | 67.1 | 61.4 | 56.0 | 52.4 | 50.2 |

| Modified Investment (% of Nominal GNI*) | 19.2 | 20.7 | 21.0 | 21.1 | 21.9 |

Revisions from previous Quarterly Bulletin (percentage points) | | | | | |

| Modified Domestic Demand | 0.0 | 0.0 | 0.4 | 0.3 | 0.1 |

| Gross Domestic Product | 0.0 | 0.0 | -4.0 | 2.2 | -1.2 |

| HICP | 0.0 | 0.0 | 0.6 | 0.2 | 0.1 |

| Core HICP | 0.0 | 0.0 | 0.6 | 0.3 | 0.1 |

Quarterly Bulletin No. 2 2026: Boxes

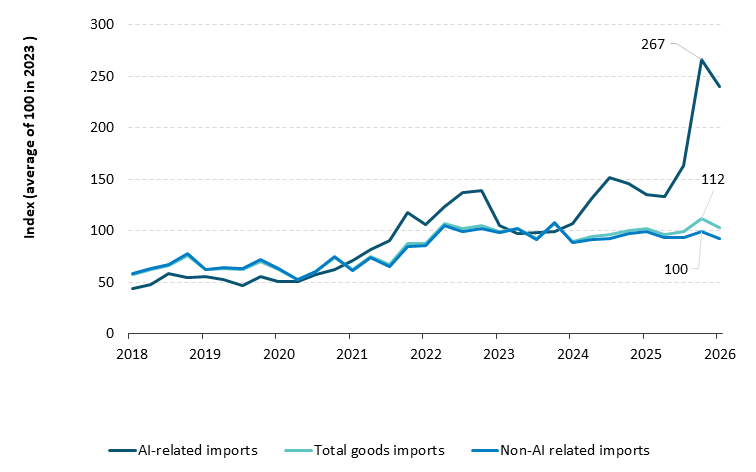

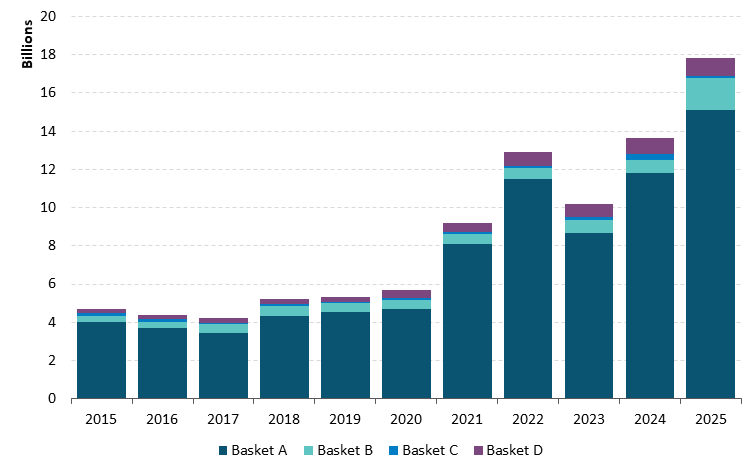

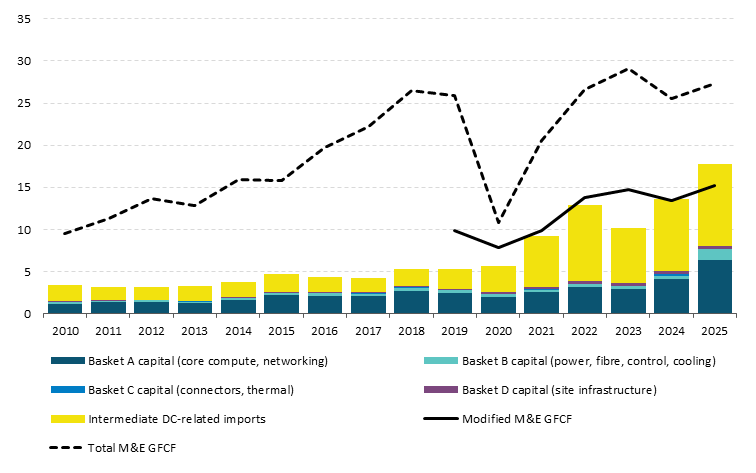

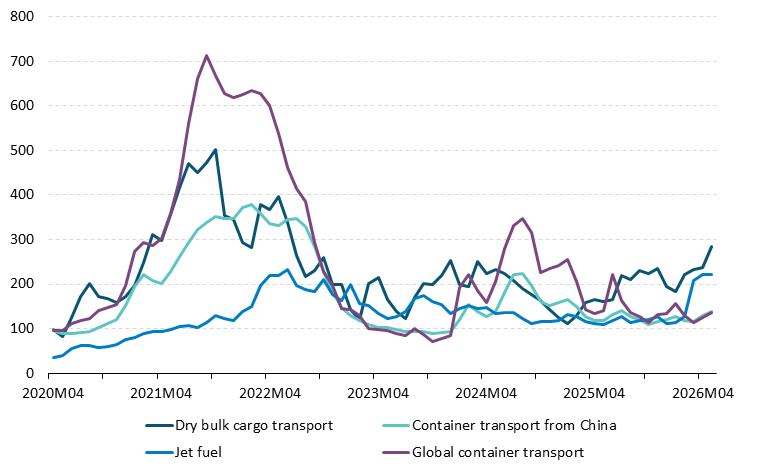

Modified machinery and equipment (M&E) investment reached €15.2 billion in Ireland in 2025, the highest level on record. The adoption of artificial intelligence (AI) and the continued expansion of data centre activity in Ireland have been mentioned

as factors contributing to the recent growth in investment. Since much of this type of investment is imported, an examination of more granular import data can reveal the magnitude